The high-tech real estate startup boasts SoftBank backing, a $1.6 billion war chest, and plenty of skeptics

marker.medium.com

How Compass Became the Bane of Real Estate

The high-tech real estate startup boasts SoftBank backing, a $1.6 billion war chest, and plenty of skeptics. Now it’s cashing in on the pandemic real estate boom.

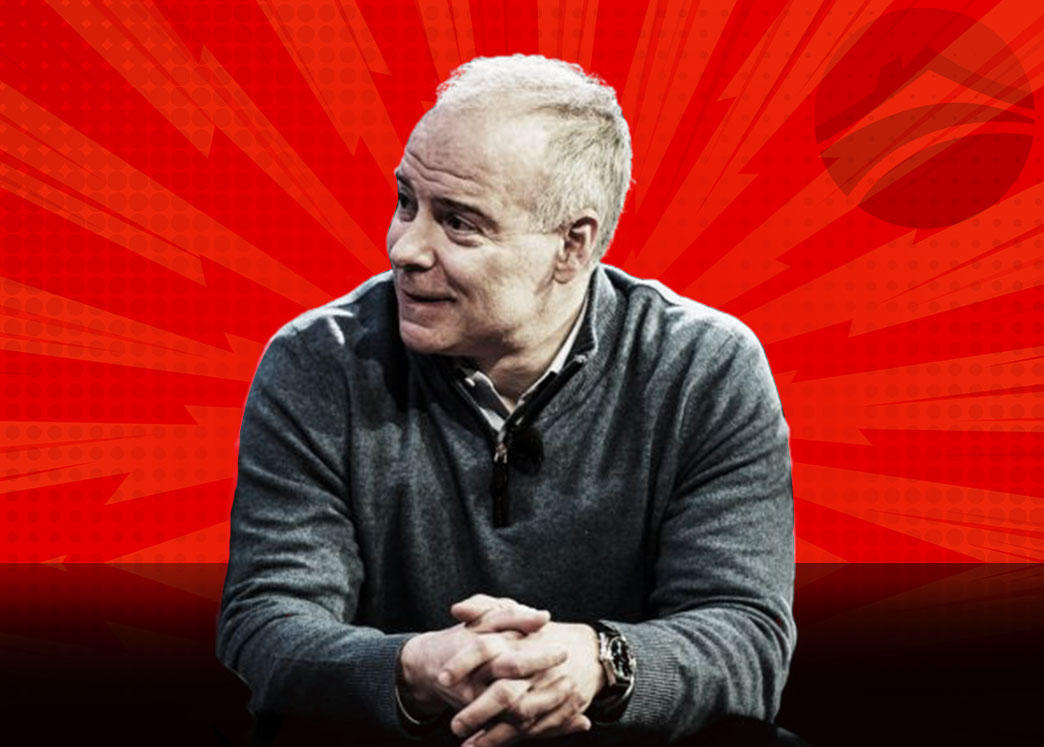

“None of us knows how long this crisis will last,” pleaded Robert Reffkin in a

letter to Nancy Pelosi and her Republican counterpart Kevin McCarthy in March. Reffkin, CEO of real estate startup Compass, was urging Congress to include independent contractors

like real estate agents — some 2 million of them in the United States, according to the National Association of Realtors — in its economic stimulus package. In his plea, Reffkin cleared up any misconceptions about the professionals: They were entrepreneurs and small business owners who represent the backbone of the U.S. economy, personify the American dream, yet typically only earn less than $41,800 per year. “We do know that for real estate agents, the economic pain will last even longer than it will for those in many other professions.”

The heartfelt missive on the plight of his industry during a pandemic — he even mentioned his mother, who works as an agent for his firm — came during a particularly bleak moment for Compass and its more than 11,500 independent contractor agents who depend on it. With the backing of $1.6 billion in venture capital, including a

$450 million infusion from SoftBank in December 2017, Compass had been on a growth streak, grabbing market share in the nation’s most expensive housing markets and becoming a major player in high-end residential real estate. But as everything, including real estate sales, ground to a halt in late March, it left a commission-dependent workforce desperate for signs of life.

Reffkin sent his letter on a Thursday. The following Monday, he laid off

375 of his full-time staffers, characterizing the moment as an “economic standstill” and forecasting a 50% revenue decline over the next half a year. By mid-April, after stay-at-home orders and shutdowns froze the economy, new weekly home listings in New York City, one of the company’s largest markets, were

down 89% year over year. Worries of hollowed out,

abandoned urban centers began to take hold, a particularly grim scenario for a luxury urban real estate company.

By this summer, Compass hadn’t just recovered, it was posting record-breaking monthly revenue every month from June to October.

While the

urban exodus story was largely a myth, wealthy families would begin relocating to bigger, more spacious homes,

or purchasing second homes. All of this made Reffkin’s letter seem as dated as a sepia-toned dispatch in a Ken Burns documentary. By late spring, home buying had started to swing back with a force no one had anticipated. Since then, real estate sales, particularly expensive single-family homes, have been booming,

hitting a 14-year high in October, per the National Association of Realtors, the same month the number of homes on the market priced over $1 million doubled and the median home price jumped 15%, setting a record high.

By this summer, Compass hadn’t just recovered, it was posting record-breaking monthly revenue every month from June to October. In June, July, and August, agents netted 50% more revenue than the same period last year. Since April, it has

brought on 3,500 more agents to meet demand. Compass competitor Redfin found that luxury home sales, defined as homes in the top 5% in the market, are up 42% year over year in the third quarter of 2020, and showings, both virtual and in-person, have skyrocketed in recent months,

up 64% year over year in September. The surge has been most pronounced at the highest end. “New listings for what we define as affordable homes is up just 2.8% in Q3,” says Daryl Fairweather, chief economist at Redfin. “For luxury, inventory is up 45%.”

Now, rapidly expanding during a historic upswing in home buying, Compass is using its billion-dollar war chest to build on that momentum with new technology and its army of agents. Compass, first launched as an apartment rental site called Urban Compass in 2012 co-founded by Reffkin and serial tech entrepreneur Ori Allon, is aiming to build a brokerage with the valuation of a tech giant.

With the SoftBank backing and massive valuation, there have also been no shortage of Compass comparisons to WeWork.

While well-funded upstarts taking aim at large established industries is nothing new, few asset classes boast the value of U.S. homes, worth

more than $30 trillion dollars. Compass’ strategy has been to develop what its chief technology officer Joseph Sirosh told

Marker is an “operating system” for the antiquated real estate industry. Things like bespoke customer relationship management tools that use predictive A.I. to tell agents who and when to target; computer vision and machine learning to examine pictures of your home and tell you what upgrades you need to make to increase the sales value; and a slick smartphone app that lets an agent create customized video clips for social media to help one client sell their home, send a bottle of champagne to another happy customer, and generate and send itineraries for tomorrow’s home tour, all in minutes. The aspiration is that with every agent interaction tracked, it will eventually be able to recommend which strategies work best. “The nature of our platform is that it’s like Shopify or Salesforce,” says Sirosh.

The narrative of the tech-first disruptor is a well-tread path.

Salad giant Sweetgreen, which has

raised nearly half a billion dollars, has shown the value of casting itself as a technology firm that just happens to sell lettuce. While Compass is currently valued at $6.4 billion, it’s been met with skepticism, often withering, especially from established industry players. Its valuation is

10 times that of Realogy, the giant conglomerate of marquee firms such as Sotheby’s and Coldwell Banker that dominates the U.S. real estate market and has almost six times more annual revenue and 20 times more agents.

When asked by business journalist Andrew Ross Sorkin why it appears that his company is actually seeing growth from rolling up small and large real estate firms as opposed to tech investment, Reffkin responded with the pithy “Is Amazon a retailer or tech company? Is Uber a transportation or tech company?”

With the SoftBank backing and massive valuation, there have also been

no shortage of Compass

comparisons to WeWork. (While Reffkin and Allon declined to speak to

Marker, Compass fiercely resists those comparisons, underscoring that unlike the co-working giant,

it has no debt.) According to

The Real Deal, Compass

has acquired more than a dozen brokerages, including a San Francisco-based firm with $14 billion in annual sales. It expanded from 37 to 122 markets in 2018, reportedly seducing brokers with unsustainably high commissions. A real estate executive in New York City who doesn’t compete with the firm says the startup’s greatest strength isn’t technology — but good old-fashioned brute force. “They’re a disruptor by capital, not innovation,” he says. “It’s amazing it’s gotten this far. They’re a brokerage that doesn’t offer anything different; they’re just better at selling an idea.”

Real estate has largely defined

the history of America, from land grabs and westward expansion to the growth of cities, suburban sprawl, and today’s McMansions. But the actual realty profession is little more than 100 years old, born, according to Jeffrey Hornstein, author of

A Nation of Realtors, of the early 20th century progressive-era drive to encourage entrepreneurship and escape the yoke of corporate servitude.

Beginning in the late 19th century, real estate salesmen created professional groups as a reaction to the dubiousness of the then relatively unregulated career path. Prospective sales agents, nicknamed curbstoners, would compete by placing multiple signs and placards in front of a for-sale property brimming with modern conveniences, the public left hoping to choose an agent with scruples. It was an “open listing” market filled with speculators; a seller could work with as many agents as they wanted to, only paying the one who brought them a buyer.

Realtors saw professionalization as a route to more sales and less consumer skepticism, and pushed a narrative of moral salesmanship to the public. The home, according to Hornstein, was fast becoming a focal point of consumerism, and consumers needed expert guidance to find the right one. To help combat the reputation of agents as bamboozling sharks, realtors pushed for state licensing requirements and formed multiple listing services; sellers would offer agents exclusive rights to their property and pay them commission for sales.

Throughout the economic booms and busts, the hot market of the 1920s, and the vast post-WWII homebuilding spree, realtors would continue evolving their business practices and organizational structure, taking advantage of the government’s explicit backing of homeownership as an economic good (one that was, and still is, severely restricted for people of color). Before the Great Depression, a down payment for a home may have been as much as half the home’s value. But the New Deal and postwar boom in government loan programs, revolution in credit availability, and dramatic increase in supply due to suburbanization and a booming economy meant that consumers saw their paychecks rise while

home prices stayed relatively flat between 1950 to 1970. By 1928,

one in every 80 Californians had a real estate license.

Over the past 50 years, the two biggest factors upending real estate was the cultural obsession with it — and the internet.

While marketing methods would change, a formalized industry began to take shape. In 1925, a broker in Fort Wayne, Indiana, had a “brand-new sales idea” to show completely furnished homes. In the ’30s and ’40s agents created sales networks so they could show prospective buyers multiple options. (Before, it was typically one agent moored to a single home.) In 1952, a realtor in Dallas began using the model house concept, to sell the future vision of a home. Century 21, founded by a pair of Orange County agents in 1971, set out to create the franchise “McDonald’s of real estate” model. Alongside firms like Coldwell Banker, initially founded in 1906 in San Francisco, Century 21 would rapidly expand in the ’70s and ’80s, corporatizing and scaling the franchise model, comprised of independent contractors as agents, to improve sales and salesmanship. In the ’80s, brokers would provide access to

MLS books, huge, telephone-directory-like collections of local listings agents would thumb through for listings, often making photocopies to take into the field.

Over the past 50 years, the two biggest factors upending real estate have been our increasing cultural obsession with it — and the internet. Beginning in 1999, Home and Garden Television began airing

House Hunters, the first in a long series of shows featuring what writer Kate Wagner, who founded

McMansion Hell, called “

sledgehammer-driven makeovers,” and the underlying idea that smart renovations can inflate values and transform property. (The home-flipping boom would soon follow.) Zillow, which launched in 2006, became a portal of real estate information and an

aspirational time-suck for millions, one in a wave of websites and services that would democratize access to real estate data.

Where realtors previously were experts with rarified knowledge and insider information, by the 2010s, they were mostly engaged in customer service and facilitation, less oracles and more operators and advisers connecting buyers and sellers (though they still

make relatively the same commission amount they did decades ago, according to a 2019 Brookings study, a nice cut when average home prices have skyrocketed). During a

2006 interview, Zillow founder Richard Barton said, “Realtors currently sit at the middle of the transaction. I think in the future they will sit more on the outside offering specific services.”

But the process — endless paperwork, applying for mortgages, working with inspectors and escrow, and, yes, the old-fashioned signs — make it seem behind the times, lending a car salesman vibe.

This sidelining has only been compounded by what real estate tech investor Clelia Peters has coined “the white T-shirt problem” — a consumer is more heavily tracked and analyzed, and experiences a more technologically savvy checkout process, when they purchase a plain shirt, she argues, than when they make the most expensive and potentially consequential purchase of their lives: a home. And then there’s the diminishing reputation of the profession. Top residential real estate brokers are skilled professionals, juggling million-dollar-plus deals in certain markets. But the process — endless paperwork, applying for mortgages, working with inspectors and escrow, and, yes, the old-fashioned signs — make it seem behind the times, lending a car salesman vibe. It makes sense that in 2020, young brokers, given the choice between an old-school established real estate firm and a hot tech company, will probably choose the latter.

All of this made the industry a prime target for Ori Allon, an Israeli-Australian serial entrepreneur and computer scientist. Allon had sold companies he’d founded to both Google and Twitter, each boasting proprietary technology that became core parts of how both tech giants operated. (In 2005, when he was 25 pitching to Google in San Francisco, he started by saying, “I’ll show you the

future of the world of search.”) He used some of the proceeds to buy his hometown basketball team — Hapoel Jerusalem — a perennial also-ran, and turn it into a championship contender. Along with Reffkin, a former chief of staff for the president of Goldman Sachs and White House Fellow who ran nearly 50 marathons, who he met during dinner at an American Academy of Achievement conference, Allon launched Urban Compass in 2012.

Allon initially saw the real potential in real estate in the data. There are more than 600 versions of the Multiple Listing Service, the shared data platform that lists homes for sale, across the country. Allon believed that by bringing all these data sources under one roof, creating a system that could parse and analyze, seeing trends faster than a human agent, he could create a more efficient, and ultimately more lucrative, sales process. In 2014, he told the

New York Times that he loves to “fix things with technology, and real estate needed to be fixed.” It was a challenge “way more interesting to me than what I’ve done in the past,” and his target demographic was “every person that can operate an iPhone or website.”

Allon’s vision for a real estate tech company did tap into a colossal problem faced by the industry. The work of agents is very inefficient. As M. Ryan Gorman, CEO of Coldwell Bankers (part of Realogy), puts it, they are the “quarterback of every transaction,” and responsible for so much marketing and prospecting work that happens out of the eyes of a consumer. Coordinating with escrow companies, prepping homes for showings, creating marketing material, scheduling tours, and even setting up renovations can add hours of work before factoring in face-to-face conversations with clients. But Gorman says both consumers and agents had been resistant to taking the human touch out of the largest transaction most of them will ever make.

In 2018, the firm, flush with SoftBank funding, launched a massive acquisition campaign in cities across the country, poaching agents with the goal of grabbing 20% of 20 markets by 2020.

Other tech companies had already digitized pieces of the process. Whereas Zillow made home values more accessible and transparent, and Redfin created a digital-first brokerage, Compass, bolstered by technology, would aim to make the sales process more efficient. To get there, Allon and Reffkin swung in a bunch of directions. Initially, the firm touted its agent-side technology. Then, in 2016, it launched an app for consumers that provided agents and buyers and sellers constantly updated market information. The company would continue to ping-pong back and forth between being an agent-focused and consumer-centric platform, eventually settling on trying to be all things to all people. Now, according to Rory Golod, president of Compass’ New York region, the platform is “B-to-B-to-C” (business to business to consumer), with the agent at the center.

Compass began with an $8 million seed round in 2012, with investments from Goldman Sachs and Founders Fund, among others, and by 2016, had raised $208 million with a valuation of $1 billion. In 2018, the firm, flush with SoftBank funding, launched a massive acquisition campaign in cities across the country, poaching agents with the goal of grabbing 20% of 20 markets by 2020. Candy Evans, a Dallas-based publisher who runs a local real estate news site

CandysDirt, says that “high-end brokers were quaking in their boots, and everyone perked up” when Compass came to town. Agents tend to prefer firms with more expensive property and better commission splits, which enable them to make more money on each sale. This was especially important amid increased competition: The National Association of Realtors found that while the number of brokers nearly doubled from 760,000 in 2000 to 1,359,000 in 2018, the number of total transactions actually dropped, from 5.99 million to 5.96 million.

Across the country, agents spoke about getting generous fee splits from Compass, or signing bonuses some rumored to be in the seven figures. Compass said they do not poach; Realogy, which has a

pending lawsuit in New York accusing the company of just such an action, disagrees. Matt Spangler, Compass’ chief marketing solutions officer, says Compass’ retention rate is the best in the industry, and they’re “not paying people any more money than anybody else.” (“You’re not poaching anyone; you’re attracting someone,” he clarifies.) Investor Peters, who sits on the board of trustees of Side, a VC-backed brokerage in San Francisco, says that an explicit part of their strategy is to lock up as many good agents as they can for as long as they can, so the ecosystem of other options for them will be limited. “Is that innovation?” she says. “To me, that seems more scorched earth.”

But agents like Evans say that while Compass’ aggressive splits and signing bonuses work in the moment, agents are mobile by nature, and when one- or two-year contracts are up, they often return to their old firms. She believes the spree of acquisitions, bonuses, and favorable terms is about market share, more than anything else. “You can keep your revenue split at 90 or 95%, what agent wouldn’t want to go there?” she says. In Dallas, Compass took on legacy firms such as Briggs Freeman and Ebby Halliday, and now, according to Evans, are on nearly equal footing. “They did find the agents,” she says, “but here’s the rub: How are you going to turn a profit when you’ve given them almost all of their commission? They have a beautiful office. Their marketing has expensive signs. But how are you going to turn a profit?”

At the end of 2018, Compass made a splashy hire with its new CTO, Sirosh, Microsoft’s former CTO of artificial intelligence who had also created a fraud detection system for Amazon. He’s helped introduce Compass Lens, which determines which upgrades will raise the sale price the most, and the custom CRM software that tells agents when it’s better to get in touch with contacts. He’s opened up Compass tech campuses in Seattle and India and hired hundreds of coders and A.I. experts to help improve Compass’ technology, all while the company has gone on an acquisition tear, buying up Contactually (customer management), Detectica (A.I.), and Modus (digital title and escrow services, core parts of a real estate transaction).

Over Zoom in mid-October, Sirosh explained that Compass’ technology could handle all the grunt work, with agents doing more transactions with less cost, and reach more customers with Amazon-level service quality. As co-founder Allon — who has no day-to-day role at Compass, but currently serves as executive chairman —

once said, “bringing the science to what has for too long been only an art.”

Tony Accardo has been a realtor for the last 12 years, working the Los Angeles beachfront and Palos Verdes. He saw Compass as the only player that’s “looking forward, not backwards” in an often stodgy business. When the company came to L.A., he saw them growing at such a fast pace, he told his wife, “If I don’t do this, I’m going to miss the train.” He joined in 2018 and now 90% of his day is spent behind the Compass dashboard, looking at market data, seeing which properties his clients click on. It’s a “portal that provides everything, cohesively branded and well thought out.” He says it makes him much more efficient with his time, and his 2020 sales are triple what they were last year.

Victor Lund, a real estate tech consultant, says that as Compass continually adds more data points to better understand the market and its clients, it’ll create a longer-lasting relationship with the high-end buyers and sellers making up an increasingly large part of the market. “In terms of raving fans, Compass agents we speak to often refer to their CRM and marketing tools as the best they have encountered,” he says. “I tend to agree. Compass has already passed their peers who have fumbled quite significantly in the core tools provided to agents, but the next iterations of Compass tech that leverages data as an asset to improve agent effectiveness and client services will reveal an entirely new landscape for the industry.”

Lund believes other tech solutions for real estate — Keller Williams’ A.I.-powered virtual assistant Kelle, for example, which is focused on teams and associates, and

various iBuyer options, which use an algorithm to place a competitive bid on a property — just aren’t as focused, and loyal, to the agent as the one being built by Compass.

But when pressed for specifics and stats to confirm the effectiveness of its technology, Sirosh won’t go beyond vague. When asked if he had data on how the agent tools impacted sales and performance, he noted that the top third of agents are growing at amazing rates year over year, but “it’s hard to say whether it’s correlation or causation, but either way, it’s a good story.” Could he provide more details, or hard numbers or statistics that proved the efficacy of Compass technology? Sirosh suggested the company was growing too fast, and changing so quickly, it was hard to quantify. “It’s all good and positive and big numbers, but with hockey stick growth in the number of agents, there’s limited history around any specific thing. Meanwhile, a

multilayered study by real estate tech expert Mike DelPrete from this spring showed that on an array of different measures, from production to transactions, Compass agents lagged behind the competition.

If there were a ubiquitous symbol of real estate in need of a high-tech reimagining, Compass believed it was the for-sale sign sitting on someone’s front lawn.

J Maggio, a top-producing agent with Conlon, a Chicago boutique firm that operated in the city and nearby suburbs, was courted by Compass in 2017, says he got the “horse-and-pony show,” but turned them down, only to become a Compass agent in 2018 when they bought out his firm. “I’ll say this as politely as I can: Compass had a cool software presentation, but none of it saved me time, made me extra money, or made my life easier,” he says. The tech he used until he left the firm in March of this year was worse than what he’d used at other brokerages. “Compass has a young, swaggy vibe, but the tech wasn’t fully baked for what I needed it to be.”

If there were a ubiquitous symbol of real estate in need of a high-tech reimagining, Compass believed it was the for-sale sign sitting on someone’s front lawn. “The real estate sign, for years, was very stagnant, a missed opportunity,” says Johan Liden, an industrial designer at Aruliden, a global design firm hired by Compass in 2017 for the makeover. “It needed to be a true icon that people can interact with.”

When Compass unveiled the reinvented sign in the summer of 2018, it seemed like the perfect totem of the rapidly expanding brokerage: A sleek, black extruding aluminum wand, backlit by LED lights and wired with an accelerometer, temperature sensor, and Bluetooth connectivity, it announced, like an upside-down exclamation point, that the house was a must-see — walk right up, scan a QR code, and take a virtual tour with your phone.

Fast Company hailed Compass for the innovation, which was set to hit the front yards of its properties that fall.

But it never made it past the first batch of 1,000 signs. Which was probably a good thing. “I thought a $1,000 digital sign was a waste of money,” says Maggio, the Chicago broker who left Compass this past March after two years. “This was like the show

Silicon Valley where an idea really doesn’t need to be improved upon; it’s for the wow factor.”

As Compass tries to make the financial case for its technology-juiced business model — with the eventual goal of taking the company public, which

Reffkin indicated in September — it needs to prove it’s more than just flashy packaging. “What’s happening now with the acquisitions and the scrambles is they’re attempting to reposition themselves as a tech company,” says investor Peters. “Is the market going to buy that story?”

The first wave of post-pandemic home buying was more impulsive, with families jumping to the suburbs looking for more space. But as time goes on, and the pandemic continues, and decisions about remote work and lifestyles may harden, Redfin’s Fairweather expects more and more buyers to make a move. She points to Sacramento as a key example; it’s long been attractive to Bay Area residents looking for a cheaper, more spacious home, and saw a massive spike in high-end sales, 86% year over year across the metro area. As people look for more long-term housing solutions, she thinks smaller, secondary markets like this may be more popular, such as Portland, Oregon, or West Palm Beach, Florida.

Brokers say the suburbs are on fire. In the New York region, the Hudson Valley, Long Island, Westchester, and the Hamptons are seeing homes disappear as soon as they go on the market. Maggio in Chicago says this luxury buying spree means a lot of the larger, older suburban homes — McMansion-like properties that may have gone out of style in the rush toward downtown — are suddenly in demand. “This is as liquid as the market is going to be,” he says. “There’s a big push by agents to get people to sell because buyers are coming from the city, and homes need to be on the market now.”

Meanwhile, Reffkin, who purchased his new home in New York City during the pandemic, is as bullish as ever about his city’s housing market. While Manhattan’s office space continues

to empty out — it hasn’t had this much available since 2003 — Reffkin believes that as soon as the vaccine arrives, companies and workers will change their tune. Plus,

he says Compass’ elite slice of the market is continuing to boom — at least for now. “In the $20 million-plus listing market we’re seeing more activity driven by wealthy and savvy investors looking for opportunity, and in the sub-$2 million market, we’re seeing a font of new first-time buyers being driven by record low interest rates,” he recently told CNN. “And they want to take advantage of it while it lasts.”

www.wsj.com

www.wsj.com