Fed balance sheet will be over 10-12trln by end of 2022If you were alone on a deserted island surrounded by salt water, you've got a couple of coconuts and a chest with $1 billion dollars in cash, are you rich or are you poor?

#wealth #mmt #Fed

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Where is mortgage money going to come from?

- Thread starter David Goldsmith

- Start date

Long term unemployment rises:

www.cnbc.com

www.cnbc.com

Treasury yields rise:

www.cnbc.com

www.cnbc.com

Stimulus seems a sure thing:

www.nytimes.com

www.nytimes.com

Welcome to MMT.

Long-term unemployment is close to a Great Recession record

Almost 40% of unemployed workers have been out of a job for at least six months. That means many have entered a particularly risky period of joblessness.

www.cnbc.com

Treasury yields rise:

U.S. Treasury yields rise as unemployment rate dips

The jobs report comes after stronger-than-anticipated data on U.S. jobs markets in recent days and amid hopes of another coronavirus relief package.

www.cnbc.com

Stimulus seems a sure thing:

House Puts $1.9 Trillion Stimulus on Fast Track, With No G.O.P. Votes (Published 2021)

“I see enormous pain in this country,” said President Biden, who is pushing forward with his plan over Republican objections. Democrats advanced with plans to begin drafting the aid package next week and speed it through the House by the end of the month.

Welcome to MMT.

MBS Live Recap: Panic In The Bond Market

Panic In The Bond Market It's no mystery that longer-term Treasury yields have been trending higher since August (it's all we can talk about at times) and that mortgage rates have largely been able to ignore that trend. But that blissful ignorance is...

www.mortgagenewsdaily.com

MBS Live Recap: Panic In The Bond Market

Panic In The Bond MarketIt's no mystery that longer-term Treasury yields have been trending higher since August (it's all we can talk about at times) and that mortgage rates have largely been able to ignore that trend. But that blissful ignorance is increasingly hard to maintain--a fact that hits home on days like today. For a variety of reasons, today was a big bad day for Treasuries. As feared, MBS were painfully unable to outperform, and the same can be said of mortgage rates compared to MBS prices. Bottom line: rates rose sharply. Multiple lenders repriced for the worse. This is part of an ongoing, widespread reevaluation of economic and monetary outcomes as told by the bond market. There's no guarantee that things get better before they get worse.

Jobless claims show unexpected move higher

First-time filings for jobless claims totaled 861,000 last week, above the Dow Jones estimate of 773,000.

www-cnbc-com.cdn.ampproject.org

www-cnbc-com.cdn.ampproject.org

Jobless claims show unexpected move higher

First-time filings for unemployment insurance jumped last week in a sign of continuing strife for the labor market.New claims totaled 861,000, the highest level in a month and above the Dow Jones estimate of 773,000, the Labor Department reported Thursday.

Markets moved little on the news, with stocks opening lower on Wall Street.

The total for the week ended Feb. 13 marked only a slight uptick from the 848,000 a week earlier. That number was revised up from the initially reported 793,000.

Continuing claims declined again, edging lower to just below 4.5 million, a drop of 64,000. That data runs a week behind the headline first-time claims total.

The total of those receiving benefits dropped by 1.3 million to 18.34 million, primarily due to a falloff in those on Covid-19 pandemic-related claims in the final week of January. However, those numbers have accelerated in early February.

"We're still at the mercy of the virus, so it's still a bifurcated economy," said Liz Ann Sonders, chief investment strategist at Charles Schwab.

Several states saw large increases in claims last week, led by Illinois with 33,491 and California's 20,657, according to unadjusted data. Texas saw a drop of 12,428 while Rhode Island was off 6,269.

Jobs data remains the weak link in an economy that otherwise has shown much stronger-than-expected gains to start the year. Retail sales surged in January thanks to pandemic relief checks that Congress authorized in December, and most other data points have defied outlooks for a weak first half of 2021.

Congress is trying to negotiate a $1.9 trillion White House stimulus plan. Part of that proposal includes extended jobless benefits that are scheduled to run out in mid-March.

A separate report Thursday saw January housing starts fall 6%, more than expected, but building permits surged 10.4%, easily above Wall Street estimates.

Foreclosures 2021: What to Expect in the Months Ahead

Editor's note: This piece originally appeared in the February 2021 edition of DS News. The million-dollar questions that everyone in the industry is asking right now are: “What are foreclosures going to look like once the foreclosure moratoria and forbearance programs come to end? And will we...

dsnews.com

dsnews.com

Foreclosures 2021: What to Expect in the Months Ahead

The million-dollar questions that everyone in the industry is asking right now are: “What are foreclosures going to look like once the foreclosure moratoria and forbearance programs come to end? And will we see all those borrowers in forbearance end up in default?”The short answer is “there probably won’t be a foreclosure tsunami.” But mortgage servicers and other default servicing professionals should prepare themselves nonetheless. Some industry analysts have predicted a huge wave of foreclosures once the forbearance program comes to an end. Popular opinion at the start of the pandemic was if there were 4 million people in forbearance, we’d ultimately have 4 million people in foreclosure. But the way the program has worked so far suggests that’s simply not the case. The Federal Reserve Bank of St. Louis estimated that 500,000 borrowers avoided foreclosure during the fourth quarter of 2020 due to coordinated relief efforts, which makes the CARES Act forbearance program is one of the best examples we’ve ever seen of the government and the industry working hand-in-hand to accomplish such a positive outcome.

The program has done exactly what it was supposed to do: allowed millions of people to get through the pandemic and recession without losing their homes while giving them time to get back on their feet financially once COVID-19 is under control. But there are still millions of borrowers in the forbearance program. What will happen to them as they exit, and how will the industry handle the high volume of borrower requests for repayment plans?

Forbearance and Foreclosures in 2020

As of the end of 2020, about five and a half percent of active mortgages—about 2.7 million loans—were in the forbearance program, down from over 8% at its peak in March. That represents a large number of borrowers for servicers to deal with as they exit the program, but it doesn’t necessarily mean that an equally large number of foreclosures will follow.

The data, in fact, suggest just the opposite: as people have exited forbearance, they’ve done so successfully. According to Mortgage Bankers Association research, from July 2020 when borrowers began exiting the program through the end of the year, about 87% of them did so with a repayment plan in place, their loans reinstated, their missing payments deferred to the end of the loan, paid off the loan, or had a loan modification in place—all positive outcomes.

The remaining 13% of homeowners who left the program without a repayment plan of some sort in place are the ones who are probably most at risk of going into default. If these numbers remain consistent, about 325,000 people will exit the forbearance program over the next six to nine months without a plan in place. Some—but probably not all—of those loans will likely default.

Prior to the pandemic, foreclosure activity was running at about half of its normal rate. In a normal year, about 1% of loans are in some stage of foreclosure. In early 2020, it was between 0.5% and 0.6%, so loan quality was very high and loan performance was twice as good as normal. There were about a quarter-million loans in foreclosure when the pandemic hit. Presumably, most of them have been protected by the moratoria but all of those will eventually be coming back into the pipeline pretty rapidly once the moratoria are lifted.

To put these numbers into perspective, if we take the 250,000 loans that were in foreclosure prior to the pandemic and assume all 325,000 of the borrowers exiting forbearance without a plan in place will default, there would be 575,000 loans in foreclosure—a foreclosure rate of 1.15%, barely above the historic average, and a far cry from the 4% of loans in foreclosure at the peak of the Great Recession.

What's Different in 2021?

That said, suggesting that there won’t be a significant increase in default activity in 2021 would be silly. It’s almost impossible to see a scenario where 40 million Americans lose their jobs and foreclosure rates don’t increase. As we move through 2021, there are a number of things that could inflate the number of defaults.

Unemployment: Before the pandemic, unemployment rates were at 3.5%, the lowest they’d been in 50 years. At the end of 2020, unemployment rates had come down from nearly 15% during the first wave of the pandemic to about 6.8%, roughly twice the pre-pandemic rate. Assuming that unemployment stays around that level, it wouldn’t be unreasonable to suggest that foreclosure activity might also double, under normal circumstances. That would take the foreclosure rate from 0.5% back up to its normal level of about 1% of all mortgages.

But the majority of jobs lost during the COVID-19 recession were concentrated in a handful of industries —travel, tourism, hospitality, retail, restaurants—and those industries tend to have young, hourly wage employees with relatively low homeownership rates. So the impact of job losses to-date has been much more severe among renters than homeowners, which could keep foreclosures from spiking.

Given the nature of the job losses, there could be markets more susceptible to defaults than others—markets heavily dependent on some of the hardest-hit industries. Markets like Las Vegas or Orlando, which are both almost entirely built on travel, tourism, and entertainment, are probably going to be the hardest hit.

Commercial Defaults: The nature of this recession, with certain industry segments being decimated, also means that we’ll probably see more distressed inventory in the commercial sector than we see in a more typical recessionary cycle. The retail and hospitality segments, in particular, will suffer in the short term.

Retail was already struggling before the pandemic, and the shelter-in-place orders and government-mandated business closings have already taken a toll on the industry. The plight of suburban malls has been well chronicled over the past few years, and the recession has accelerated their demise in many markets, but thousands of smaller retail facilities and restaurants have gone out of business in the last year, creating many more distressed properties in the process.

In the hotel segment, a surprisingly large number of smaller, limited-service hotels are owned by small-to-mid-sized investors, who may not have the financial strength to survive an extended downturn. Occupancy rates in 2020 lagged behind 2019 by 40% and showed no signs of near-term improvement. Even a number of large hotels, like the historic Roosevelt Hotel in New York City, have shut their doors, and may find themselves in the foreclosure rolls in 2021.

The Rental Market: There’s also likely to be some short-term disruption in the apartment or multifamily sector due to the recession and the eviction bans put in place by the federal, state, and local governments. There are a lot of building owners in those sectors who are highly leveraged and who are unable to collect rent right now since their tenants are out of work—a toxic combination, which will probably lead to some distressed rental properties hitting the market.

The single-family rental (SFR) market so far hasn’t suffered much from missed rent payments, but that could change if the recession continues or worsens. Over 90% of SFR properties are owned by mom-and-pop investors without the deep financial pockets of institutional investors. An uptick in job losses among their higher-income renters, or the expiration of government stimulus and enhanced unemployment benefits could result in more defaults among these rental property owners.

Why Defaults May Not Lead to Foreclosures

When borrowers default on a loan, it’s not unusual for the default to be resolved before the foreclosure. Loans are re-instated or refinanced, or the property is sold and the debt retired before the foreclosure auction. For financially distressed homeowners today, market dynamics provide a much better environment than what we saw during the last recession.

A primary difference this time is that homeowner equity is at an all-time high: over $6.5 trillion. According to RealtyTrac’s parent company ATTOM Data, about 70% of homeowners have more than 20% equity. Other published research has indicated that more than 90% of borrowers in forbearance have more than 10% equity in their properties. Homeowners with ample equity in a housing market characterized by historically low inventory of homes for sale, historically low mortgage rates and strong demand should be able to sell their properties—perhaps at a modest discount—in order to avoid a foreclosure. So even as we see the number of defaults increase as the forbearance program ends and foreclosure moratoria eventually expire, the record level of homeowner equity means that the overwhelming majority of distressed assets are likely to be sold well before the foreclosure auction.

Those same market dynamics also favor mortgage servicers and noteholders who find that foreclosure is the only option for some of their borrowers. Investors are eager to purchase properties at foreclosure auctions or as REO assets on the open market, and use sites like RealtyTrac to find, analyze, and target properties they plan to fix-and-flip or buy-and-rent. Competition between traditional homebuyers, individual investors, and institutional investors should drive up sales prices and shorten hold times, which helps servicers minimize losses for their clients.

The biggest challenge for default servicing professionals is going to be effectively managing the enormous volume of borrower contacts—and the subsequent loss mitigation processes associated with millions of delinquent loans—once the government moratoria and forbearance programs expire. Staying compliant with frequently changing state and local foreclosure regulations will add a layer of complexity as well.

The bottom line is that although the number of foreclosures is unlikely to approach the levels seen in the Great Recession, there’s a huge wave of default activity coming that will wipe out servicers who don’t plan ahead and make sure they have the people, processes, and technical resources ready to meet the challenge.

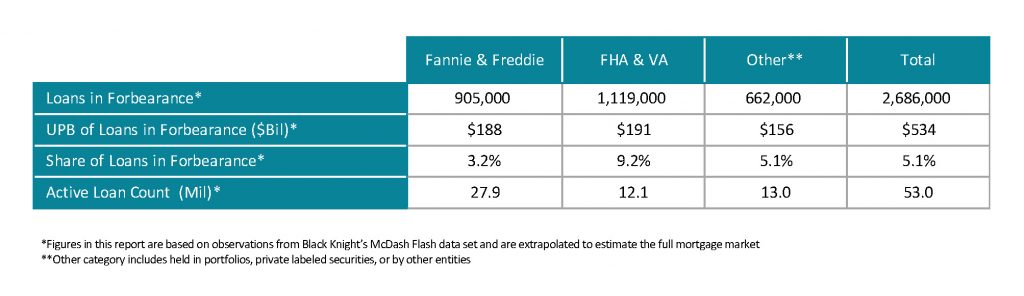

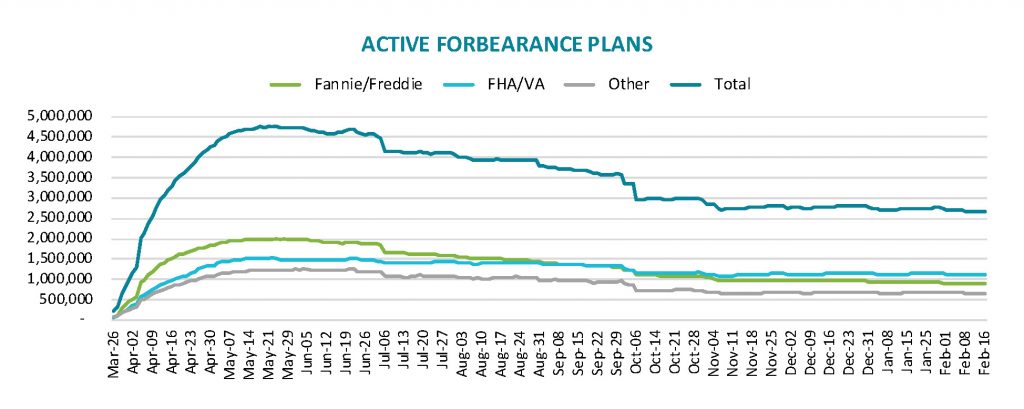

Active Forbearance Numbers Trending Upward

Black Knight has released the results of its latest McDash Flash Forbearance Tracker, finding that the trend of mid-month forbearance increases continues to rise. Black Knight has found that the number of active forbearance plans increased by 15,000, a 0.6% rise over last week, with...

dsnews.com

Active Forbearance Numbers Trending Upward

Black Knight has released the results of its latest McDash Flash Forbearance Tracker, finding that the trend of mid-month forbearance increases continues to rise.Black Knight has found that the number of active forbearance plans increased by 15,000, a 0.6% rise over last week, with portfolio-held and privately securitized mortgages accounting for the largest weekly increase at 12,000 (1.8%). FHA/VA forbearances saw an increase of 5,000 (0.4%), while the GSEs experienced slight improvement, with a decrease of 2,000 forbearance plans (-0.2%).

As of Feb. 16, 2.69 million U.S. homeowners remain in forbearance, with 9.2% of that number representing FHA/VA mortgages, 3.2% GSE mortgages, and 5.1% portfolio/privately securitized mortgages.

As Black Knight’s Andy Walden notes, with the month of February coming to a close, nearly 204,000 forbearance plans are scheduled to expire, suggesting that any decline in forbearance volumes in the coming weeks is likely to be limited.

Despite the weekly increases, the overall monthly rate of decline held steady at -2% month-over-month. This continues the trend of very slow, but consistent, improvement in the number of outstanding forbearance cases. New plan starts hit a post-pandemic low this week, while just one of every 77 homeowners who entered the week in forbearance left their plans.

Should the federal government not take any further action to assist struggling U.S. homeowners, more than 600,000 seriously delinquent borrowers will reach the end of their allotted forbearance periods at the end of March.

“The vast majority of plans have a 12-month cap on payment forbearance, and the various moratoriums which have kept foreclosure actions at bay over the past 10 months may be lulling us into a false sense of security about the scope of the post-forbearance problem we will need to confront come the end of March,” said Black Knight Data & Analytics President Ben Graboske in an earlier release. “Last year saw the largest number of homeowners—nearly 3.6 million—become 90 or more days past due since 2009, and as of the end of December, 2.1 million remained so.”

Mortgage Rates in U.S. Reach Highest Point Since July

Applications for loans to buy homes increased last week as rates reached a seven-month high, the Mortgage Bankers Association reported.

therealdeal.com

Mortgage rates surge — and refinance applications sink

Despite higher costs, applications for purchase loans increased 2% last week

Requests for loans to buy homes increased last week as mortgage rates hit their highest point since July.An index tracking applications to purchase homes increased 2 percent, seasonally adjusted, from the prior week, according to the Mortgage Bankers Association.

The uptick came despite rates rising to their highest point since July 2020 in the biggest one-week gain in almost a year, according to Joel Kan, head of industry forecasting at MBA.

The average rate for a 30-year, fixed-rate mortgage increased to 3.23 percent, up from 3.08 percent. The rate for jumbo loans rose 10 basis points to 3.33 percent.

“Mortgage rates jumped last week on market expectations of stronger economic growth and higher inflation,” said Kan in a statement. He blamed the increase for the lack of growth in applications to refinance.

MBA’s index tracking refinancing requests increased 0.1 percent last week from the week prior. It marked the fourth week of overall decline in the share of refinancing requests, which still account for the majority of loans in MBA’s weekly indices.

The average size of purchase loans fell for the first time in six weeks, despite rising home prices. Kan attributed the decline to a jump in government mortgage applications, which are likely first-time homebuyers with smaller budgets.

Last week’s average purchase loan was $412,300, down from $418,000 the week before.

MBA’s survey covers 75 percent of the residential mortgage market and has been conducted weekly since 1990.

Cash-Out Refinancings Hit Highest Level Since Financial Crisis

Home prices have soared during the coronavirus pandemic, prompting more borrowers to pocket cash from refis.

www.wsj.com

www.wsj.com

Cash-Out Refinancings Hit Highest Level Since Financial Crisis

Home prices have soared during the coronavirus pandemic, prompting more borrowers to pocket cash from refis.

www.wsj.com

Cash-Out Refinancings Hit Highest Level Since Financial Crisis

Mortgage rates just moved sharply higher, but homebuyer competition is fiercer than ever

Mortgage rates bounced sharply higher again this week, making homebuying even more expensive at the start of the all-important spring market.

www-cnbc-com.cdn.ampproject.org

Mortgage rates just moved sharply higher, but homebuyer competition is fiercer than ever

- Mortgage rates bounced higher again this week, making homebuying even more expensive at the start of the all-important spring market.

- With home prices skyrocketing, any rise in rates knocks even more potential buyers out of the running, and yet somehow the housing market is more competitive than ever.

With home prices skyrocketing, any rise in rates knocks even more potential buyers out of the running, and yet somehow the housing market is more competitive than ever.

The average rate on the 30-year fixed mortgage hit its last low of 2.75% at the end of January, and has since climbed pretty steadily, according to Mortgage News Daily. After a sizeable move overnight, it now stands at 3.45%.

"Since the beginning of February, the total damage is nearly 3/4ths of a percent, making it one of the biggest moves in any 6 weeks, ever," said Matthew Graham, chief operating officer at Mortgage News Daily.

"The purchase market always weathers these storms, and the ultra-tight supply situation coupled with still-ravenous demand in many metro areas may keep the housing market surprisingly buoyant. The bigger question is when rising rates will ultimately impact prices."

CNBC Real Estate

Read CNBC's latest coverage of the housing market:

Mortgage refinance demand tanks 39% as rates continue to climb

The housing market stands at a tipping point

The rate is the same now as it was a year ago. The difference from a year ago, however, is that home prices are soaring.

Prices are now up over 10% from this time in 2020, according to CoreLogic, and there appears to be no letup in the gains. This is due to the record low supply of homes for sale.

Homebuilders are not stepping up as much as hoped, because they are facing higher costs for land, labor and materials. They also continue to experience delays in getting materials to job sites, due to Covid. Single-family housing starts came in much lower than expected in February, and the backlog of unbuilt homes is rising.

"There has been a 36% gain over the last 12 month of single-family homes permitted but not started as some projects have paused due to cost and availability of materials," said Robert Dietz, chief economist of the National Association of Home Builders. "Single-family home building is forecasted to expand in 2021, but at a slower rate as housing affordability is challenged by higher mortgage rates and rising construction costs."

New homes already come at a price premium to existing homes, so rates are particularly important to that market.

For a new home with an estimated median price of $346,757 in 2021 and the recent 30-year fixed-rate mortgage rate of 3%, a quarter percentage point increase in the interest rate would price out approximately 1.3 million households, according to a new calculation by the NAHB.

The supply crunch of existing homes is only exacerbated by higher mortgage rates. Homeowners who sell would likely have to buy their next home at a higher interest rate, so that's a significant deterrent to moving.

The number of newly listed homes for sale for the week ended March 13 was 24% lower year over year, according to realtor.com. The total number of homes for sale is now half of what it was a year ago.

While this situation makes it harder for buyers, it also shows that buyer demand has not fallen off much, even in today's higher rate environment. If buyers had fallen back, the supply would be rising.

Buyers are in fact, "flooding the housing market early this year, eager to find a home of their own," according to Danielle Hale, realtor.com's chief economist. On average, homes are selling seven days faster than last year.

Housing demand was pulled forward last year. The pandemic created an emotional need to nest, not to mention a practical need for more space, given the work- and school-from-home environment. Even as vaccinations rise and more people go back to offices and schools, homebuyers are still not only out in force but are increasingly competitive.

Just over a third of homes sold in February went for more than their original asking price. That is the largest share on record, according to Redfin, a real estate brokerage.

"This is the strongest seller's market since at least 2006," said Daryl Fairweather, Redfin's chief economist. "Buyers outnumber sellers by such a huge margin that many homeowners are staying put because they know how hard it would be to find a place to move to."

Mortgage rates rise again, making refinancing less attractive for many homeowners

Mortgage rates climbed for the fifth week in a row, dampening the purchasing power of home buyers and further winnowing the pool of candidates who can benefit from refinancing into a lower rate.

Mortgage Demand Falls to Lowest Level in a Year

Mortgage demand fell in April to its lowest level in almost a year, according to Inman citing a report from the data firm Black Knight

therealdeal.com

Mortgage demand plummets to lowest level in a year

Cash-out refinancings were down 13% month-over-month

The once red-hot mortgage market is cooling down.Mortgage demand fell in April to its lowest level in almost a year, according to Inman, citing a report from the data firm Black Knight.

The reason: refinancings have fallen off. Cash-out refinancings were down 13 percent from March to April, while rate-and-term refinancings plummeted 20 percent, per the report. Black Knight says there are 14.5 million homeowners who could still refinance their existing mortgage at a lower rate.

Lower demand for refinancings has caused purchase loans to take a larger share of the market. Those made up 55 percent of total originations in April, up from 52 percent in March, according to Black Knight.

Historically low mortgage rates have been the norm for some time now, but that may soon end. Economists at Fannie Mae project rates on 30-year fixed-rate mortgages to reach 3.4 percent by end of 2021 and then rise to 3.6 percent in 2022. That’s up from 3.1 percent last year.

Lenders have also been tightening their standards in the past year. Overall, mortgage credit availability — an indicator for lenders’ willingness to issue mortgages — is at its lowest level since 2014, according to recent data from the Mortgage Bankers Association.

Last year, mortgage rates plunged to historic lows, encouraging would-be buyers into the market and spurring refinancings. (Rates have since gone up.) But the availability of loans dropped 35 percent year-over-year as lenders tightened standards to avoid lending to buyers with shaky finances.

Mortgage rates rise to 3% as the Fed mulls a shift in policy: 'Their path forward is quite uncertain'

Mortgage rates are still low by historical standards.

Mortgage rates jumped higher in response to hints that the Federal Reserve may soon alter its approach to the economy in light of high inflation.

The 30-year fixed-rate mortgage averaged 3% for the week ending May 20, up six basis points from the previous week, Freddie Mac FMCC, -1.01% reported Thursday. It’s the first time in roughly a month the benchmark mortgage rate has touched the 3% mark, but it remains below where it stood at the end of March when it reached the highest level since June of last year.

The 15-year fixed-rate mortgage increased three basis points to an average of 2.29%. The 5-year Treasury-indexed adjustable-rate mortgage averaged 2.59%, the same as a week ago.

https://eb2.3lift.com/pass?tl_click...0&bcud=18750&sid=66552&ts=1621556037&cb=13637

The mortgage market hiked rates as investors responded to the first indications from the Federal Reserve that the central bank may begin taking steps toward scaling back the policies put in place to help the economy through the coronavirus pandemic.

The Fed released the minutes from its April meeting, which noted that multiple officials “suggested that if the economy continued to make rapid progress toward the committee’s goals, it might be appropriate at some point in upcoming meetings to begin discussing a plan for adjusting the pace of asset purchases.”

‘Mortgage rates are still very low by historical standards, but their path forward is quite uncertain.’

— Matthew Speakman, an economist with Zillow

The news sent the yield on the 10-year Treasury note higher — mortgage rates roughly track the direction of long-term bond yields, including the 10-year Treasury TMUBMUSD10Y, 1.634%.

“Mortgage rates are still very low by historical standards, but their path forward is quite uncertain,” said Matthew Speakman, an economist with Zillow ZG, +3.73% Z, +3.66%. (They 30-year rate exceeded 18% as the Fed attempted to get a handle on runaway inflation in the early 1980s.)

“Markets will surely be keeping a close eye on any signals that the Fed may be closer to tightening policy, which in previous recessions has sparked a strong increase in rates.”

Among the assets that the Fed has been purchasing to stimulate the economy are mortgage-backed securities. By purchasing these securities, the Fed pumped liquidity into the mortgage market that allowed lenders to drop rates to attract applications. Without that source of liquidity, though, lenders would need to increase rates.

Until the Fed’s exact policy change is certain, mortgage rates could become much more volatile. But even if rates do move higher, home buyers don’t necessarily need to worry about affordability constraints just yet.

For starters, an average of 3% on the 30-year fixed-rate mortgage is extremely low by historical standards. As the economy begins to open up more and more from the restrictions put in place to stem the tide of the pandemic, that should give another breath of life into the real-estate market.

“Business activity and real estate traffic are ready to embrace the new post-pandemic normal,” said George Ratiu, senior economist at Realtor.com. “This will boost the number of homes for sale, offering buyers more choice and slowing the steep price growth we’ve seen over the past 10 months.”

Traders eye Fed pullback on mortgage bonds

Housing boom gives central bank less reason to support market

Mortgage traders have eyes on the Federal Reserve’s purchasing of mortgage bonds.With the housing market booming and lending rates still low, suspicions are growing that the Fed will no longer keep buying $40 billion worth of mortgage bonds every month, Bloomberg News reported.

Federal Reserve Could Dial Back on Mortgage Bonds

The booming housing market may lead the central bank to scale back on its purchasing of mortgage bonds.

therealdeal.com

Fed Officials Debate Scaling Back Mortgage-Bond Purchases at Faster Clip

Soaring home prices lead some officials to call for the central bank to stop buying mortgage bonds sooner than Treasury bonds

Redirecting

www-wsj-com.cdn.ampproject.org

Another section of the market which "we're never going to see again" since we learned our lesson with 2008 GFC.

JPMorgan invests in private-label mortgage platform

With Maxex, the banking giant looks to revive a forgotten sector of the mortgage market

JPMorgan Invests in Private-Label Mortgage Clearinghouse

JPMorgan Chase is the latest company to invest in the “private label” mortgage sector,

therealdeal.com

Biden ousts Fannie, Freddie overseer, leaving them in government’s hands

The move comes after the Supreme Court ruled the FHFA’s structure unconstitutional

Investors who bet that Fannie Mae and Freddie Mac would soon be privatized have another thing coming.

The Biden administration ousted the head of the Federal Housing Finance Agency after the Supreme Court ruled that its current structure is unconstitutional, the Wall Street Journal reported.

FHFA Head Ousted: Fannie, Freddie Remains in Gov’t Hands

Biden administration removes Federal Housing Finance Agency head Mark Calabria, who had pushed to end government control of Fannie Mae and Freddie Mac.

therealdeal.com

As Housing Prices Peak Zero Down Mortgages are Back: No Down Payment Loans Available up to $1.25 Million.

www.doctorhousingbubble.com

www.doctorhousingbubble.com

As Housing Prices Peak Zero Down Mortgages are Back: No Down Payment Loans Available up to $1.25 Million.

The attention span of people is slightly above that of a cat thanks to social media platforms that rewire the brain for instant gratification, including on the financial front (think of all of the meme stocks and Robinhood). All the cheerleading that is happening for real estate is largely

www.doctorhousingbubble.com

Does anyone know where that "tick tock" sound is coming from?

Total household debt – mortgages, HELOCs, credit cards, auto loans, student loans, and other debt – jumped by $313 billion in Q2, from Q1, according to the New York Fed’s Household Debt and Credit report today. This 2.1% jump was the biggest quarter-over-quarter jump in years, matching Q4 2013, and both were the biggest jumps since 2007. The total balance of debt reached nearly $15 trillion.

...

But forbearance for federally-backed mortgages, after having been extended, is running out this fall. At the end of Q2, there were still nearly two million mortgages in forbearance. To exit forbearance, the borrower will sell the home and pay off the mortgage, or the lender will refinance the mortgage often with lower payments and extended terms to make it easier for the borrower to pay for.

This is all part of a gigantic government-backed extend-and-pretend scheme that includes eviction bans for renters – now expired at the federal level but not at state and local levels – and student loan forbearance, still scheduled to expire at the end of September.

This is an economy where credit problems have been swept under the rug, where many consumers stopped making payments without negative consequences, even as free money hailed down upon them.

Because delinquencies are no longer delinquencies but count as “current,” credit scores rose on average – and in the process, credit scores have become useless for banks to determine the creditworthiness of a potential borrower.

After 16 months of sweeping this stuff under the rug, there is now a huge mess under the rug, and the temptation in government is to just keep it there and forget about it, or have the taxpayer clean it up, rather than consumers, lenders, and investors.

State of the American Debt Slaves: Forbearance & Free-Money Phenomenon amid Soaring Prices of Homes & Autos

Mass-forbearance is the best thing that ever happened to sweeping reality under the rug. But now, there’s a huge mess under the rug.

To the Fed’s great relief, hardy American debt slaves are finally going deeper into debt, after having made unnerving efforts in prior quarters at paying down their credit cards, the most expensive debts with the biggest profit margins for banks. What helped push up total borrowing were massive price increases that had to be financed – particularly homes and vehicles – and the loans to finance these purchases jumped even if the volume of purchases didn’t.Total household debt – mortgages, HELOCs, credit cards, auto loans, student loans, and other debt – jumped by $313 billion in Q2, from Q1, according to the New York Fed’s Household Debt and Credit report today. This 2.1% jump was the biggest quarter-over-quarter jump in years, matching Q4 2013, and both were the biggest jumps since 2007. The total balance of debt reached nearly $15 trillion.

...

But forbearance for federally-backed mortgages, after having been extended, is running out this fall. At the end of Q2, there were still nearly two million mortgages in forbearance. To exit forbearance, the borrower will sell the home and pay off the mortgage, or the lender will refinance the mortgage often with lower payments and extended terms to make it easier for the borrower to pay for.

This is all part of a gigantic government-backed extend-and-pretend scheme that includes eviction bans for renters – now expired at the federal level but not at state and local levels – and student loan forbearance, still scheduled to expire at the end of September.

This is an economy where credit problems have been swept under the rug, where many consumers stopped making payments without negative consequences, even as free money hailed down upon them.

Because delinquencies are no longer delinquencies but count as “current,” credit scores rose on average – and in the process, credit scores have become useless for banks to determine the creditworthiness of a potential borrower.

After 16 months of sweeping this stuff under the rug, there is now a huge mess under the rug, and the temptation in government is to just keep it there and forget about it, or have the taxpayer clean it up, rather than consumers, lenders, and investors.

Another avenue of pre-GFC risk taking on the rise.

www.wsj.com

www.wsj.com

New Appetite for Mortgage Bonds That Sidestep Fannie and Freddie

Wall Street firms are again packaging and selling mortgages that the government-backed firms can’t or won’t back.

www.wsj.com