As the housing market cools, more buyers are “taking their time and exploring their options.”

finance-yahoo-com.cdn.ampproject.org

Homebuyer’s remorse: Thousands of Americans are backing out of signed contracts — what you need to know before you cancel a purchase

Sigrid Forberg

January 9, 2023, 7:00 am

Homebuyer’s remorse: Thousands of Americans are backing out of signed contracts — what you need to know before you cancel a purchase

The housing market is cooling as homebuyers contend with increasing interest rates and high prices — and some are even pulling out after they sign the dotted line.

About 60,000

home purchase agreements fell through in October, according to RedFin. That’s the most on record since the real estate brokerage started tracking that data in 2013.

Deal cancellations and price cuts also hit record highs as prospective buyers moved more tentatively following the

biggest mortgage-rate jump in over four decades.

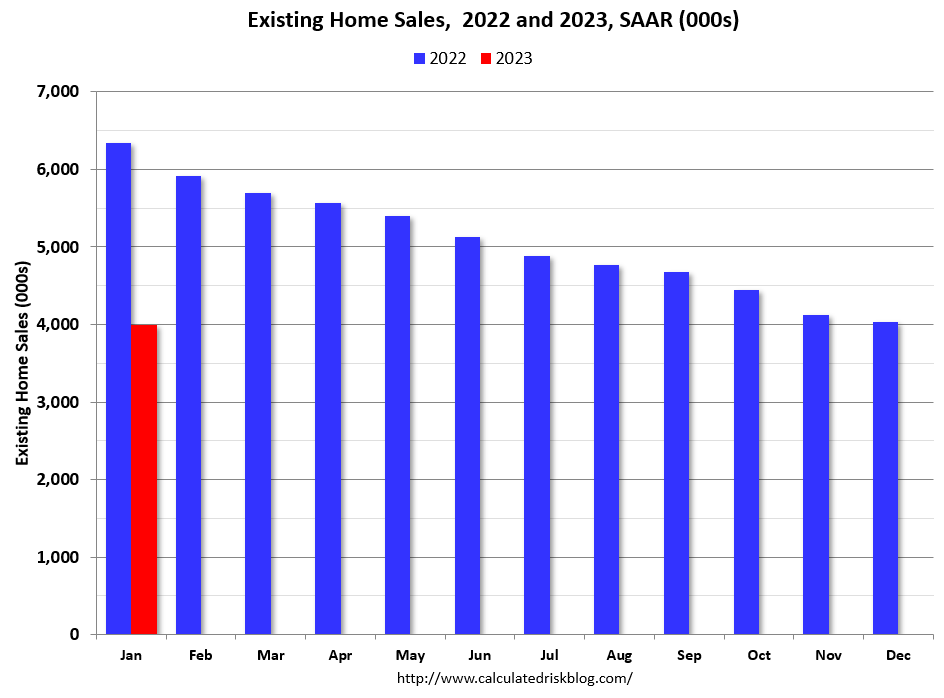

While Redfin noticed a slight decrease in canceled purchase agreements in November, home sales in general dropped to their lowest rates since 2012. Buyers at every stage of the process are clearly having second thoughts about this massive commitment.

Once you’ve made an offer on a home and the seller has accepted it, there are still a few steps before the house is officially yours.

From the time an offer is accepted and when it goes through, you’ll be in a limbo period called “under contract.”

Here’s what you need to know if you decide you want to back out of the deal.

Once you’ve made an offer on a home and the seller has accepted it, there are still a few steps before the house is officially yours.

From the time an offer is accepted and when it goes through, you’ll be in a limbo period called “under contract.”

Here’s what you need to know if you decide you want to back out of the deal.

What does it mean when a house is under contract?

Making an offer that's accepted is just the middle of a real estate transaction, not the end. And homebuyers can afford to be choosier now as demand and competition softens.

“House hunters today are taking their time and exploring their options, whereas six months ago, they had to act quickly and pull out every stop to compete because homes were selling almost immediately,” says Tzahi Arbeli, a Redfin real estate agent in Las Vegas.

“Homebuyers now will agree to buy a house and be doing the inspection, and then back out because they found another home they love more.”

When you

buy a home, this period when you’re under contract allows you to clear any conditions you wrote into the offer, like if you said your bid was contingent on your ability to get financing.

The contract is a legally binding purchase agreement, but the seller is still allowed to show the home, and other potential buyers can prepare backup offers in case the deal falls through.

However, the seller can’t drop out of the contract simply if a better offer than yours comes along.

Can a buyer back out of an accepted offer?

If you or the seller can’t meet the contract contingencies for the sale, it will be voided and you can back out. Once you sign the contract, you’ll be given a set period of time to clear these contingencies or cancel the transaction.

Common contingency issues would be: not being able to nail down financing; finding major defects during the

home inspection; or finding out through the appraisal process that the home’s value doesn’t match the purchase price.

Home inspectors don’t usually look for lead-based paint, evidence of pests, or issues with the roof, sewers or private wells. You’ll need to hire specific inspectors for those issues if you have concerns.

And if your inspector finds evidence of dangerous problems like radon gas, mold or asbestos, additional inspections may be recommended. These can be costly issues to resolve, so it’s best to uncover them before the sale clears.

Closing on a sale also involves doing a title search. If there are any liens or bankruptcies against the property, it may not be possible to transfer the title. The search also will uncover any easements or covenants, conditions and restrictions, commonly known as CC&Rs.

If there are easements and CC&Rs that interfere with your plans for the property, those are grounds for you to back out of the contract. So if an easement interferes with where you’d install a pool or swing set, and the CC&Rs limit what you can do with your yard or how you can enjoy it, you can cancel the deal.

What if the contingencies aren’t met?

If there are significant issues that come up during the contingency process — like, say, there's water damage, or the roof needs replacing — you can go back to the seller to negotiate. They may agree to come down on the price or fix the issues before closing.

If the seller refuses, it’s within your rights to back out of the deal.

While you likely got

preapproval for a loan before making an offer on the home, financing sometimes does fall through. Your financial contingency ensures you’re not on the hook for a loan you can’t afford if you can’t secure a lender.

These are all fairly standard contingencies that will lead a home sale to fall through.

But make sure you’re aware of the timeline for meeting each of your contingencies, because they can vary. You generally have 30 days to secure a loan, but only seven to 14 to have the home inspected.

Be sure to read the fine print to be sure you won’t miss your opportunity to back out gracefully.

What if I don’t have a contingency?

When you made the offer on the home, you put down a security deposit, known as earnest money. Your earnest money shows the seller that you’re serious about buying the house.

You’ll typically pay between 1% to 5% of the purchase price, but this can shoot up to 10% depending on the market.

Backing out of a sale while you’re under contract without a contingency puts you at risk of losing your earnest money.

And the seller could even take you to court to force you to close on the home, under what’s called "specific action." Winding up in court is less common, but it’s a serious risk.

When is it too late to back out of buying a house?

After you’ve signed the contract and once the contingency period has passed, it becomes much harder to back out of real estate contracts, especially if the reason is a sudden case of cold feet.

Some states may require you to go into mediation with the seller if you have a serious dispute, in the hopes of keeping the matter out of court.

But once you’ve arrived at this point as a buyer, you’ve made it clear that you’re serious about purchasing the home.

If you need to back out and have good reasons, you should put those in writing to explain things to the seller. Ask your real estate agent to help you with the messaging on your letter.

If you’re still at odds with the seller even after mediation, you may need to bring in a

real estate attorney to help you go over your options.

Ultimately, you may lose the money you put up in earnest, especially if you don’t have a good reason for backing out. But

if you can no longer afford the home or mortgage, it’s a small price to pay in the short run to avoid an even more expensive issue of foreclosure or bankruptcy down the road.