If WeWork field for bankruptcy, experts say there are several scenarios that could play out.

therealdeal.com

What would a WeWork bankruptcy look like?

Several scenarios could play out for co-working company that recently had close to $50B in lease obligations

In April, a Manhattan landlord who leases a large space to WeWork received an email from a broker who was working on behalf of the struggling co-working company to renegotiate its office leases.

“I told him politely it’s not happening, so don’t waste your time,” the landlord said, noting that because his lease with WeWork is below market-rent, he’s comfortable taking the space back. “I’m going to play hardball.”

Brokers at Newmark Knight Frank and JLL have spent the last several weeks reaching out to WeWork’s landlords — trying to negotiate concessions on billions of dollars of leases that threaten the company’s cash flows.

WeWork had $47.2 billion worth of

lease obligations on its books as of late last year, and is reportedly looking to reduce those rent liabilities by 30 percent.

Now as Covid-19 puts further pressure on the co-working company’s bottom line, critics are raising questions about whether its business model of packing a rotating cast of strangers into tight spaces can survive in a world of social distancing and contact tracing.

That raises the stakes for WeWork’s lease negotiations, according to those who believe this could be a make-or-break scenario for the Softbank-backed company once valued at as much as $47 billion before its failed IPO last year. WeWork was recently valued at just

under $3 billion, Bloomberg reported in May.

WeWork’s critics have long speculated that the company could be forced to file for bankruptcy in a downturn. If that happened, WeWork would have several scenarios laid out in front of it, experts told

The Real Deal.

“Landlords aren’t always willing to make concessions outside of bankruptcy,” said Timothy Duggan, an attorney at the Stark & Stark in New Jersey who represented office equipment provider Transamerica as a creditor when Regus — another large flex-office company — filed for bankruptcy in 2003.

But that dynamic often changes once under Chapter 11.

“If I’m a landlord and I know a bunch of other landlords are making concessions and I have a shot of coming out of bankruptcy, I might be more willing to make a deal,” Duggan noted.

Still, under the protection of bankruptcy the company’s core challenge would be the same: It still has to convince its creditors that it has a viable plan to turn things around.

“Even in bankruptcy, they still have to get people to believe they can come out of this,” Duggan added. “It’s all still one big negotiation.”

ReWork

WeWork had $1.3 billion of long-term debt when it issued its prospectus last year, including credit agreements with JPMorgan and $669 million in corporate bonds. Those bonds were trading for as low as 28 cents on the dollar in May.

“Even in bankruptcy, they still have to get people to believe they can come out of this.” — Timothy Duggan, Stark & Stark

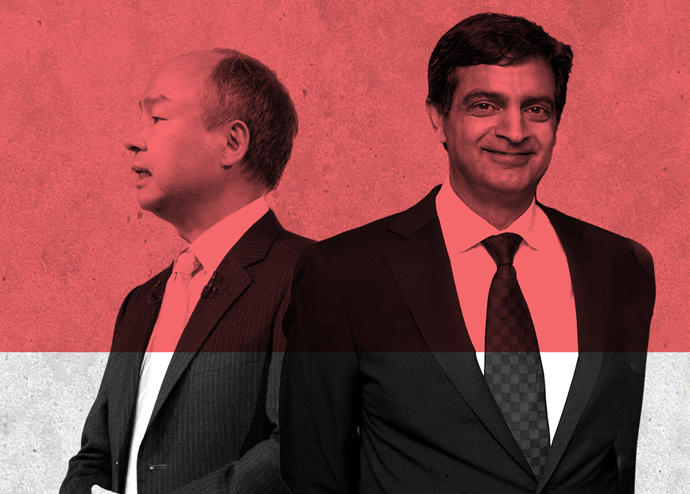

The task of convincing creditors that the company can turn itself around would fall largely on the management team headed by Sandeep Mathrani — the veteran retail executive who led mall landlord General Growth Properties through bankruptcy in 2010.

Mathrani joined WeWork earlier this year to help

right the ship after its co-founder Adam Neumann was ousted following the IPO debacle.

“He is a proven leader with turnaround expertise in the real estate industry,” SoftBank’s Raul Marcelo Claure, the former interim chairman of WeWork, said about Mathrani in a February statement.

To be clear, WeWork has made no public plans to file for bankruptcy, and that option is by no means an inevitability.

A spokesperson for the company told

TRD that WeWork has a strong financial position with $3.9 billion in cash and commitments that “provides us the liquidity to weather this current climate while also executing on our five-year plan and investing in our future.”

“We continue to rightsize our portfolio by exiting locations that are unprofitable, growing in markets where we see enterprise demand,” the spokesperson added, noting WeWork is planning to open more than 60 new locations through early 2021 and is investing $100 million in WeWork India.

But the company’s critics have long speculated that WeWork could end up in bankruptcy, particularly during an economic downturn.

The company has laid off

thousands of employees since November. Softbank backed out of a financial bailout and IBM is reportedly ready to walk from its WeWork space at

88 University Place — one of the first locations in the co-working company’s pivot to an enterprise model.

Softbank last month took another writedown on its WeWork investment, saying it expects to take a

$6.6 billion loss for the year on the portion of the firm’s stake held outside of its $100 billion Vision Fund.

“Every writedown takes Wework’s carrying value closer to reality,” Redex Holdings analyst Kirk Boodry opined in Reuters. “Clearly the value is zero.”

Softbank CEO Masayoshi Son said in April that he expects a significant portion of the 88 companies backed by more than $80 billion in venture capital from the first Vision Fund to end up in bankruptcy.

“I would say 15 of them will go bankrupt,”

Son predicted, adding that he expects another 15 of the fund’s bets to prosper.

WeWork chairman Marcelo Claure, though, sought to distance his company from those remarks.

“Make no mistake: SoftBank’s Masayoshi Son and myself are huge believers in the new WeWork and its management team, we will continue to support the company,” he Tweeted in May. “We have no doubt that WeWork will emerge from COVID19 stronger than ever and are committed to profitability by 2021.”

Mathrani said WeWork

paid rent at 80 percent of its locations in April and May and that it collected rent from 70 percent of its members. It’s difficult to gauge whether or not the Newmark and JLL brokers have been successful in negotiating the necessary concessions from building owners.

Representatives for Newmark and JLL did not respond to requests for comment.

WeWork may be able to avoid the bankruptcy route thanks to a number of leases that are reportedly held by subsidiaries with “limited parent guarantees.” That means WeWork could walk away from individual leases without triggering liability back to its parent company.

A new chapter?

But if it came to a bankruptcy situation, experts laid out several scenarios.

In Chapter 11 a tenant usually makes a binary decision on leases: It either accepts the lease or rejects each deal. Landlords who hold rejected leases get to file a claim as an unsecured creditor and divvy up whatever’s left over after the restructuring plan. They usually end up accepting pennies on the dollar for their agreements.

WeWork could have options other than up or down on leases, and the Regus case could provide a blueprint.

Duggan said that Regus got permission from the court to take a second shot at renegotiating its leases during bankruptcy, and the flex-office company was successful in reworking about 70 deals. The benefit of doing it that way, he added, is that landlords are more likely to see it as their last shot at coming away with a more favorable outcome.

“The problem outside bankruptcy is, sometimes the landlords don’t believe the company is going to file,” Duggan said.

If WeWork were to file, though, Duggan explained the company could then go to their landlords with more leverage. “Now [WeWork] can say, ‘Here’s proof; We’re in Chapter 11,’” he said.

Even if it were to play out that way, Mathrani and his team would still have to convince WeWork’s largest landlords that it could come out of restructuring with a successful plan, according to sources.

Bankruptcy experts say that in Chapter 11, a committee of unsecured creditors made up mostly of WeWork’s largest landlords would play a significant role in approving or shooting down a restructuring plan.

“The institutional landlords are really going to decide whether they believe in the plan or not,” said one attorney who spoke on the condition of anonymity because he represents one of WeWork’s landlords.

“It’s really hard to see WeWork coming out of this if they do file,” the attorney added. “In order for the company to be reorganized, its creditors have to be confident that management can execute.

WeWork’s five biggest landlords around the country, as of last summer, were Beacon Capital Partners, Nuveen Real Estate, the Moinian Group, Boston Properties and the Chetrit Group, according to data from Costar Group. A spokesperson for Beacon Capital declined to comment, and representatives for Moinian, Boston Properties and the Chetrit Group did not respond to requests for comment.

Chad Phillips, head of Nuveen’s Americas office portfolio, pointed out that the company only has 2 percent of its space exposed to WeWork. He added the investment manager believes demand for flexible office space will increase post-Covid as large office tenants move to a hub-and-spoke model.

“That said, flexible operators will need to evolve their business models and modify their formats with less density and more company control over their spaces,” he said, adding that stronger operators who can pivot in light of the pandemic stand to gain market share in the flex office space.

“A wonderful thing”

As observers watch closely, some are planning for a fallout from WeWork’s big push to reorganize.

“There’s not enough demand to support the scale of what they have. In some buildings they have 300,000 square feet when in reality they might want 60,000 square feet.” — Ryan Simonetti, Convene

Ryan Simonetti, co-founder and CEO of Convene, said he’s already been approached by office landlords who are trying to figure out what to do with their space if they take it back from WeWork.

He said Convene — which leases meeting rooms and other workspaces on a short-term basis — is considering signing its own lease deals for some of the spaces or partnering with landlords to manage them.

“We’re looking at what would it take to reconfigure a WeWork location to a Convene offering?” Simonetti noted. “There’s not enough demand to support the scale of what they have. In some buildings they have 300,000 square feet when in reality they might want 60,000 square feet.”

In the most extreme scenario, WeWork would fail to convince its creditors of a successful path forward. In that case, liquidation may be the only option.

“There’s no magic bullet here,” said attorney Hugh Ray, head of the bankruptcy practice at the trial firm McKool Smith.

“In some cases, Chapter 11 is a wonderful thing,” he added. “When it works, it’s wonderful to see. But it doesn’t work for everyone.”