Some thoughts.

The problem - Massive deflationary forces due to global shutdown from the Corona Virus. Add in a oil price war. Each on its own would be destructive. Together, its a black swan event. Health situation is scary, as everyone knows. But the financial side is even scarier. You got the shadow banking system thath is in the order of $15-20+ Trillion (no idea real number, anyone know?). Think repo markets, commercial paper, money market funds, foreign exchange reserves, eurodollars, treasuries corporate and high yield bond markets, etc etc . As revenue implodes from the shutdown, how will rents and mortgages and bills get paid for individuals, small businesses, big businesses, etc. How many will lose jobs? How many will be back at their job after this? The ripple effects are ugly. So something needs to happen and something majorly massive, far exceeding 2008/2009 credit crisis.

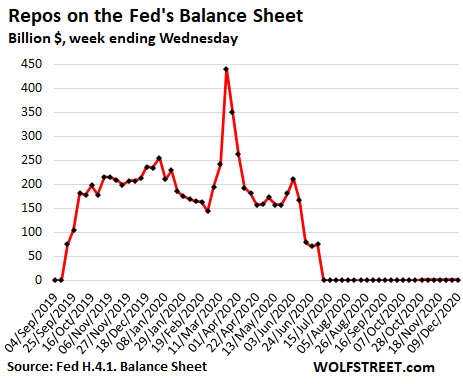

What Fed is Doing - lowered rates to zero, backstopping the banking system (especially shadown banking system/credit markets), adding trillions in liquidity to short term markets, and engaging in massive, and I mean massive, debt monetization (ie, printing money) by buying MBS & commercial MBS, ABS, Corporat Debt, Treasures, Commercial Paper, Repos, etc to primary dealers via POMO - Here is the Fed's statement from 8am this morning - https://www.federalreserve.gov/newsevents/pressreleases/monetary20200323a.htm - All of this focus is to mitigate risk of a credit event or a freeze up of the shadow banking system that will cause massive liquidations & credit shocks (think Lehman, but way worse)

What Govt is Doing - fiscal stimulus and yes it will be massive. The goal will be to give everyone $$ to bridge this situation. The problem is there will be a demand problem that we dont yet know when will return. Expect this package to be announce in phases, up to $2Trillion maybe at first with perhaps more traunches later on as needed. How will they fund this? Well normally they would issue Treasuries to fund stimulus and let the markets buy em up. But this time it seems they may order US Mint to create two, yes 2, Trillion dollar coins. I guess with the order that another coin or two may be needed in the future. So, now the Govt has these trillion dollar coins, how do they convert that to $$ to pay for this? The Fed buys the coins and mouse clicks $2Trillion into Govt accounts for use. Same thing as the Fed buying MBS and Treasuries from primary dealers via Permanent open market operations

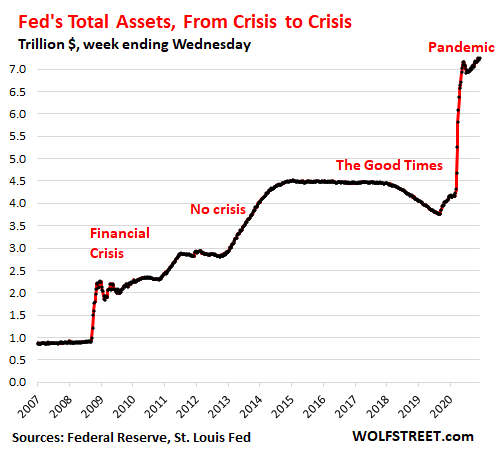

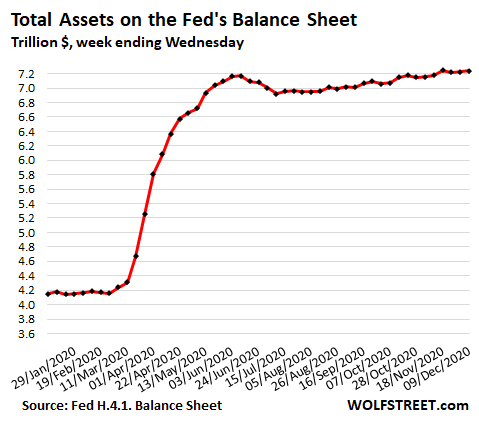

We got the Fed actions already, quite fast and insanely massive. The fiscal side is coming any day. End of day Fed balance sheet could pop to over $10trln by the time we are out of this.

We do not have an inflation problem with all this stimulus. We have massive deflationary hurricane problem that fed/govt is trying to mitigate and provide a bridge for so this doesnt turn into a depression. Its very possible unemployment temporarily spikes to 20-30% from this. Its sad to think of job losses if this goes on for longer than 1-2 months.

X Factors:

Duration until Treatment - vaccine is year away, min, so we need treatment. If we can get this approved and distributed and available and people stop dying from this, that will be huge.

Duration until Peak Containment - hugely critical. Everyone waiting for this as we know #s will surge for next 1-2 weeks as tests get reported on. How long until that curve flattens

Duration of Shutdown - hugely critical. How long does this last. It feels like markets are pricing in 1-2 months. What if its 3+ months. Praying the scientists innovate a treatment here.

Amount & Effect of Stimulus - Fed monetary is all in, and will continue be. No limits. Govt fiscal, time will tell. How does either effect this crazy cycle.

Credit Event - Will we wake up one day and have more Lehmans by the time this is done and where does that push markets?

Jobs - How does stimulus effect job losses and do we come right back after this.

So many factors as far as I see. Scary, but hoping for a positive factor to evolve...praying for treatment!

The problem - Massive deflationary forces due to global shutdown from the Corona Virus. Add in a oil price war. Each on its own would be destructive. Together, its a black swan event. Health situation is scary, as everyone knows. But the financial side is even scarier. You got the shadow banking system thath is in the order of $15-20+ Trillion (no idea real number, anyone know?). Think repo markets, commercial paper, money market funds, foreign exchange reserves, eurodollars, treasuries corporate and high yield bond markets, etc etc . As revenue implodes from the shutdown, how will rents and mortgages and bills get paid for individuals, small businesses, big businesses, etc. How many will lose jobs? How many will be back at their job after this? The ripple effects are ugly. So something needs to happen and something majorly massive, far exceeding 2008/2009 credit crisis.

What Fed is Doing - lowered rates to zero, backstopping the banking system (especially shadown banking system/credit markets), adding trillions in liquidity to short term markets, and engaging in massive, and I mean massive, debt monetization (ie, printing money) by buying MBS & commercial MBS, ABS, Corporat Debt, Treasures, Commercial Paper, Repos, etc to primary dealers via POMO - Here is the Fed's statement from 8am this morning - https://www.federalreserve.gov/newsevents/pressreleases/monetary20200323a.htm - All of this focus is to mitigate risk of a credit event or a freeze up of the shadow banking system that will cause massive liquidations & credit shocks (think Lehman, but way worse)

What Govt is Doing - fiscal stimulus and yes it will be massive. The goal will be to give everyone $$ to bridge this situation. The problem is there will be a demand problem that we dont yet know when will return. Expect this package to be announce in phases, up to $2Trillion maybe at first with perhaps more traunches later on as needed. How will they fund this? Well normally they would issue Treasuries to fund stimulus and let the markets buy em up. But this time it seems they may order US Mint to create two, yes 2, Trillion dollar coins. I guess with the order that another coin or two may be needed in the future. So, now the Govt has these trillion dollar coins, how do they convert that to $$ to pay for this? The Fed buys the coins and mouse clicks $2Trillion into Govt accounts for use. Same thing as the Fed buying MBS and Treasuries from primary dealers via Permanent open market operations

We got the Fed actions already, quite fast and insanely massive. The fiscal side is coming any day. End of day Fed balance sheet could pop to over $10trln by the time we are out of this.

We do not have an inflation problem with all this stimulus. We have massive deflationary hurricane problem that fed/govt is trying to mitigate and provide a bridge for so this doesnt turn into a depression. Its very possible unemployment temporarily spikes to 20-30% from this. Its sad to think of job losses if this goes on for longer than 1-2 months.

X Factors:

Duration until Treatment - vaccine is year away, min, so we need treatment. If we can get this approved and distributed and available and people stop dying from this, that will be huge.

Duration until Peak Containment - hugely critical. Everyone waiting for this as we know #s will surge for next 1-2 weeks as tests get reported on. How long until that curve flattens

Duration of Shutdown - hugely critical. How long does this last. It feels like markets are pricing in 1-2 months. What if its 3+ months. Praying the scientists innovate a treatment here.

Amount & Effect of Stimulus - Fed monetary is all in, and will continue be. No limits. Govt fiscal, time will tell. How does either effect this crazy cycle.

Credit Event - Will we wake up one day and have more Lehmans by the time this is done and where does that push markets?

Jobs - How does stimulus effect job losses and do we come right back after this.

So many factors as far as I see. Scary, but hoping for a positive factor to evolve...praying for treatment!