Struggling hotel owners are handing over the keys to their troubled properties but some lenders are hesitant to take them back

therealdeal.com

Underwater hotel owners are walking away from their properties

Nearly 25 % of hotel CMBS loans — roughly $21 billion — were in special servicing as of January

With its hotels business battered by the pandemic,

Ashford Hospitality Trust took a cold, hard look at its portfolio and came to a sobering conclusion: The REIT was simply going to walk away from some of its struggling properties.

“While we take no joy in handing back assets to our lenders, we do hope it demonstrates that we are willing to make hard decisions that are in the best interest of our shareholders,” Ashford CEO Rob Hays said on the company’s late-October earnings call.

Dallas-based Ashford, which was facing the threat of insolvency before it landed a $350 million lifeline right before the new year, gave up a portfolio of 13 hotels with more than 2,000 rooms as it struggled to stem losses and work out forbearance agreements to avoid defaults.

And the company warned it could soon walk away from even more properties.

Ashford isn’t the only investor making that difficult decision. Commercial real estate owners — particularly those in struggling sectors such as hotels and

shopping malls — are giving up on their debt-laden properties rather than go through the foreclosure process.

It’s reminiscent of the housing crash of 2008, when homeowners who took out big loans suddenly found that their houses were worth less than their mortgages and simply walked away from the properties. There was even a term — “jingle mail” — for owners who dropped their keys in an envelope and mailed them back to the bank.

And although the number of hotel and mall owners walking away now hasn’t reached that level, it’s a threat to consider as the mark that looms large, as many properties still struggle financially with no end in sight nearly a full year into the pandemic.

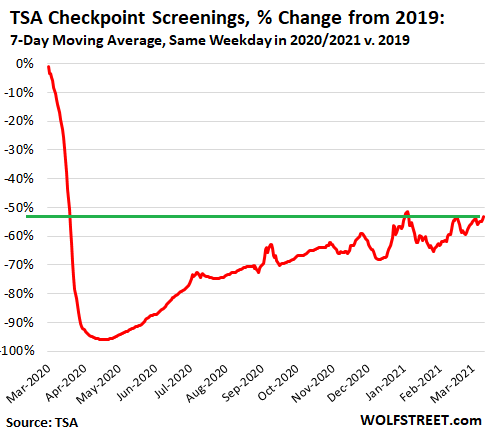

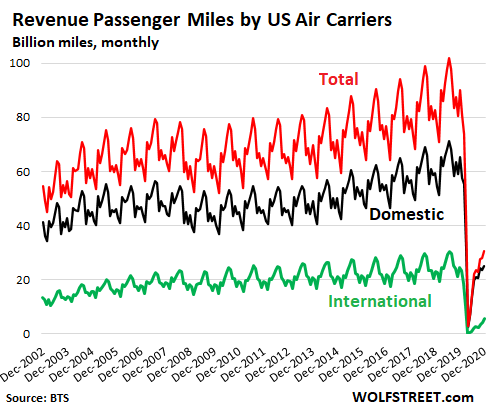

In particular, the devastation on the lodging industry over the past year is clear: As of January, nearly 25 percent of hotel CMBS loans — roughly $21 billion — were in special servicing, according to Trepp.

No reservations

In December, California-based REIT

Sunstone Hotel Investors handed over control of the 478-key Hilton Times Square to the property’s special servicer, Torchlight Investors.

The Manhattan property was in trouble even pre-pandemic, and things were set to get worse with an impending rent hike on its ground lease and its $75 million mortgage coming due this fall. Sunstone surrendered the property in a deed-in-lieu of foreclosure. It also made a $20 million settlement payment, according to servicer notes on the loan.

Other properties seem headed for a similar fate. In October, there were nearly 100 loans totaling

$3.9 billion in outstanding CMBS debt where the borrowers indicated they would be willing to hand back the keys, according to Trepp.

Homeowners may have emotional attachments to their houses that make walking away a difficult decision, but experts say that commercial owners are using the cold logic of dollars and cents.

“It’s really just a rational economic decision,” said Wendy Silverstein, co-founder of loan-workout company Silver Eagle Advisory Group. “They’re not going to be throwing good money after bad.”

In addition to the bottom line, hotel owners also have to consider their reputations with lenders when it comes to how they act in these tricky situations.

Borrowers have the option of forcing their lenders to go through lengthy and costly foreclosures, but that could be perceived as strong-arming. Owners who choose not to burn bridges with their lenders can preserve relationships for the next time they want financing, said Caroline Harcourt, an attorney at Pillsbury Winthrop Shaw Pittman who works on distressed real estate loans and restructurings.

“There’s a reason why you want to be known as someone who says, ‘Here, I’m not going to make a fuss. Take the keys,’” Harcourt said.

But some lenders can be hesitant to take properties back.

Banks prefer not to own real estate, and that makes them more willing to negotiate agreements with owners that allow them to hold onto properties. And when a bank does take back a piece of property, it helps to have a quick turnaround strategy.

Wells Fargo, for example, took control of the 239-room Fairfield Inn & Suites at 325 West 33rd Street in Manhattan last year through a deed-in-lieu from a subsidiary of the Hawaii-based investor Shidler Group. The bank turned right around and sold the property — along with its $51 million outstanding loan — to Rhode Island-based Magna Hospitality for roughly $57 million.

Unlike banks, though, CMBS special servicers are required to take over distressed properties.

And if a lender is one of the real estate operators that in recent years became more active on the debt side — particularly those in loan-to-own situations — chances are that an owner can be sitting at the negotiating table with someone who has designs on taking over the real estate.

In some cases, a lender will refuse to take back a property, which results in a standoff with an owner who has given up.

Silver Eagle ’s Silverstein said that when borrowers take out their loans, they have to spell out in writing the circumstances under which they can hand back the keys.

Smart borrowers, Silverstein said, make sure they’re covered. But a downturn usually exposes a few that forgot to read the fine print.

“Every cycle, someone seems to learn that lesson anew,” she said.

Wiggle room

Owners with properties in default are not completely out of options.

Some states have put foreclosure moratoriums in place to prevent lenders from taking properties that have fallen behind due to government-imposed lockdowns. And even under normal circumstances, foreclosure can be a drawn-out process.

In New York, for example, the average foreclosure case takes more than a year.

But in cases where the outcome is inevitable — the owner giving up a money-losing property at a foreclosure auction — handing over the keys to the lender through a deed-in-lieu can be a money saver.

“It’s a cheaper and quicker process than allowing a lender to foreclose on an asset,” Anne Lloyd-Jones, of the hospitality consulting firm HVS, wrote in an email.

But that doesn’t always mean a deed-in-lieu is the path of least resistance.

If a property has mezzanine financing, Lloyd-Jones added, a deed-in-lieu won’t wipe out subordinate liens or clear away unpaid property taxes and franchise fees. Only a foreclosure would allow the lender to get a “clean title.”

“So even though a lot of owners are voluntarily giving their keys back, sometimes the lenders are still going through the foreclosure process rather than deed-in-lieu,” Lloyd-Jones said.

On the retail front, more than 15 percent of loans were in special servicing in January, a slight improvement from the previous month. Brookfield Property Partners — among the country’s largest mall owners — recently handed over two properties to its lenders and has several

others that are at risk, according to a recent analysis of Trepp and Fitch data by

TRD.

During Brookfield’s fourth quarter

earnings call in early February, CEO Brian Kingston said that there are about 20 properties in its core retail portfolio where the malls are worth as much as the debt, and the company is considering all its options, including a deed-in-lieu giveback.

Extended stay

Strategies around distressed properties will be shaped primarily by time: How long will the economic recovery take, and do owners have enough capital to keep their hotels and malls afloat until things get better?

The vaccine rollout, which has been chaotic at times, has been improving as supplies increase, leading some in the real estate industry to express hope that things are headed back on track. Others still aren’t there yet.

Ronald Dickerman, president of Madison International Realty, said the people he knows who have been vaccinated are still behaving the way they did pre-vaccine, and they still aren’t returning to offices or traveling.

“Covid is going to be around for years,” he said.

Hotels certainly have a long way to go before they get back to pre-Covid levels. Occupancy across the U.S. was just north of 40 percent in the last week of January, according to hospitality data firm STR. Revenue per available room, a benchmark for measuring a hotel’s performance, was at slightly more than $36, about 50 percent below last year.

Chris Woronka, a hotel REIT analyst at Deutsche Bank, said that borrowers and owners have been playing something of a waiting game until it becomes clear how much economic pain each side will have to swallow.

The longer it takes, he said, the harder it becomes to keep throwing funds into money-losing properties.

“The question is, how long are you willing to wait?”