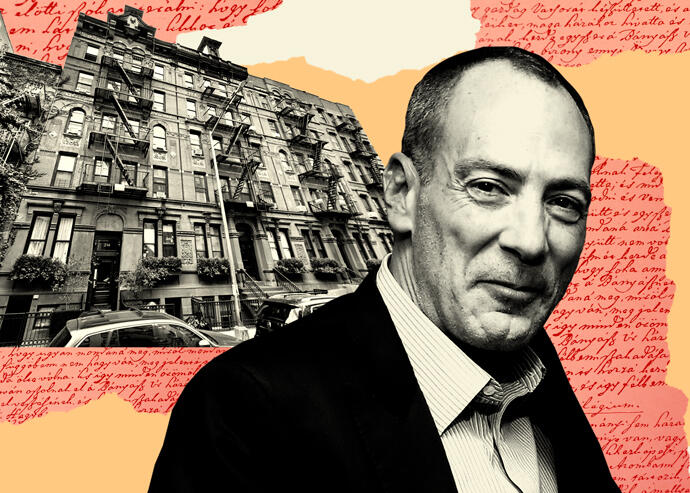

Isaac Kassirer’s Tenants Win Ruling, Launch Rent Strike

Isaac Kassirer’s attempt to deregulate six rent-stabilized apartment buildings was denied by the state this week.

therealdeal.com

Isaac Kassirer’s stuck with stabilized apartments — and rent strike

Emerald Equity loses bid to pull South Bronx portfolio from regulation

For landlords whose business model was flipping rent-regulated apartments to market rate, the 2019 rent law was crushing. The legislation closed most of those paths, dragging down the values of regulated buildings.

Some of their owners have called it quits. But others have soldiered on, trying new tactics to achieve the same result.

For one, Isaac Kassirer of Emerald Equity Group, a decision by the state last month proves that creativity isn’t enough to secure the market-rate conversions of yore.

In the late 2010s, Kassirer built up a sizable stack of stabilized assets. But the rent law brought trouble. Come December 2020, the indebted entities on more than a dozen Emerald buildings faced bankruptcy. And as of last year, the portfolio — previously 3,500 units — had shrunk by more than half.

In August 2020, Kassirer attempted to stanch the bleeding. He filed an application with the state’s Division of Homes and Community Renewal to see if six South Bronx buildings could be exempt from rent-regulation.

Kassirer argued that they had been renovated in 1991, qualifying them for the 30-year tax break known as J-51. The provision mandates that a landlord issue stabilized leases while getting the tax break. Kassirer asked the state to authorize the portfolio’s deregulation when J-51 expired last year.

Last month, the state denied the request.

HCR’s rent administrator George Nnochiri wrote in an order that each of the owner’s buildings had been rehabilitated under the city’s Urban Development Action Area Program. The incentive allows owners of buildings on land previously owned by the city to qualify for a 20-year tax break.

Nnochiri noted that the renovations had been completed via a government loan and under the state’s Private Housing Finance Law, those units are exempt from deregulation.

The decision applies to 1187 Anderson Avenue, 1191 Anderson Avenue, 1195 Anderson Avenue, 1220 Shakespeare Avenue, 1210 Woodycrest Avenue, and 1230 Woodycrest Avenue in the Highbridge section of the Bronx.

Kassirer said in an email that neither he nor Emerald Equity Group is affiliated with the Bronx properties in question. However, property records show Kassirer signed as the buyer for 1220 Shakespeare Avenue; 1187, 1191 and 1195 Anderson Avenue; 1210 Woodycrest Avenue and 1230 Woodycrest Avenue on Nov. 28, 2017.

Property records do not show any have since been sold.

Had Kassirer’s application been approved, renters in the buildings’ 272 units could have faced four-figure rent hikes and fierce competition from the open market.

But with one battle down, the renters are still waging a war for livable housing.

“The tenant association is happy about this huge victory,” said Julius Bennett, a tenant leader at 1230 Woodycrest Avenue. “But the happiness is not full.”

The buildings collectively have over 900 open violations and the city’s Department of Housing and Preservation has classified over a quarter of the infractions as “extremely hazardous.”

Tenants have complained of mice and roach infestations, leaking ceilings, mold, broken toilets and peeling lead paint, according to HPD.

And in December, residents of 1230 Woodycrest Avenue and 1220 Shakespeare Avenue received shutoff notices from Con Edison, signaling that the landlord had not paid the electric bill.

The tenants of 1230 Woodycrest, which has the most violations of the bunch, declared a rent strike Tuesday to pressure Kassirer to remedy the violations and pay Con Ed.

“The rent strike is going to go on for as long as I am old — and I’m 84,” said Bennett. “It’s going to go for as long as it takes to resolve this.”

A spokesperson for the tenants said the utility could shut off service in the common areas, which would prevent tenants from using the washer and dryer, intercom and elevator. A shutoff would also affect cooking gas and heat, the spokesperson said.

The law firm Kucker Marino Winiarsky & Bittens, which is listed as a contact for the buildings’ owner on the HCR decision, did not respond to a request for comment.

A representative for the firm previously commented on the Bronx buildings dispute on behalf of Emerald Equity Group, but later said he had done so incorrectly and had intended to send the statement on behalf of the LLCs listed as owners in the HCR filing. To his understanding, he said, neither Emerald nor Kassirer is affiliated with the properties.

and 152-09 88th Avenue (right) (Getty, Google Maps, Goldstein, Hill and West Architects)")