iBuyers and Wall Street hook up.

It’s a house, not a home: Inside the commodification of residential real estate

Is it time for the single-family home to finally act like an institutional asset?

In July, Dallas Tanner, the CEO of single-family rental behemoth Invitation Homes, announced that his company had spent $569 million buying up houses in the preceding six months. Tanner expected to roughly double that number by year-end, touting the firm’s ability to scale in its chosen markets and its portfolio’s high occupancy rates, low turnover and satisfied residents.

“Together with you, we make a house a home,”

Tanner said.

In fact, Tanner and his Wall Street and Silicon Valley-backed compatriots might be doing the opposite. If they have their way, U.S. housing — one of the country’s largest asset classes with a

total value of more than $36 trillion — will become the most mechanized, institutionalized asset there is.

Already, houses are being assessed algorithmically, marketed remotely, bought and sold in bulk and increasingly bypassing the individual homebuyer to land straight in the hands of institutional-scale landlords and investors.

The nation’s largest homebuilders and landlords are investing in iBuyers, sell-side startups that specialize in rapidly buying up homes, and the relationship is beginning to influence the ways homes are built, marketed and sold. These iBuyers, in turn, are teaming up with other venture-backed startups offering add-on services such as insurance, title and escrow, and mortgages.

Meanwhile, a growing pack of buy-side startups is enabling more transactions by using tactics seen in the auto industry, such as cash offers, rent-to-own and trade-in programs. Those startups are also getting love from builders and investors.

Fueled by cheap debt, venture capital and enormous potential profits, the home — the most emotionally resonant purchase the average American makes in their lifetime and for decades a largely peer-to-peer asset — is on its way to becoming a truly tradeable and transparently valued commodity. The implications for investors, homeowners and renters are immense.

Wall Street bets

company better exemplifies Wall Street’s shifting approach to residential real estate than Opendoor.

In August, Bloomberg reported that the iBuying pioneer,

led by CEO Eric Wu, was in talks with

lenders for a new $2 billion revolving credit facility. Opendoor wants the funds to fuel more home purchases following a whirlwind second quarter in which it more than doubled its closed acquisitions to 8,500 and placed an additional 8,100 homes under contract.

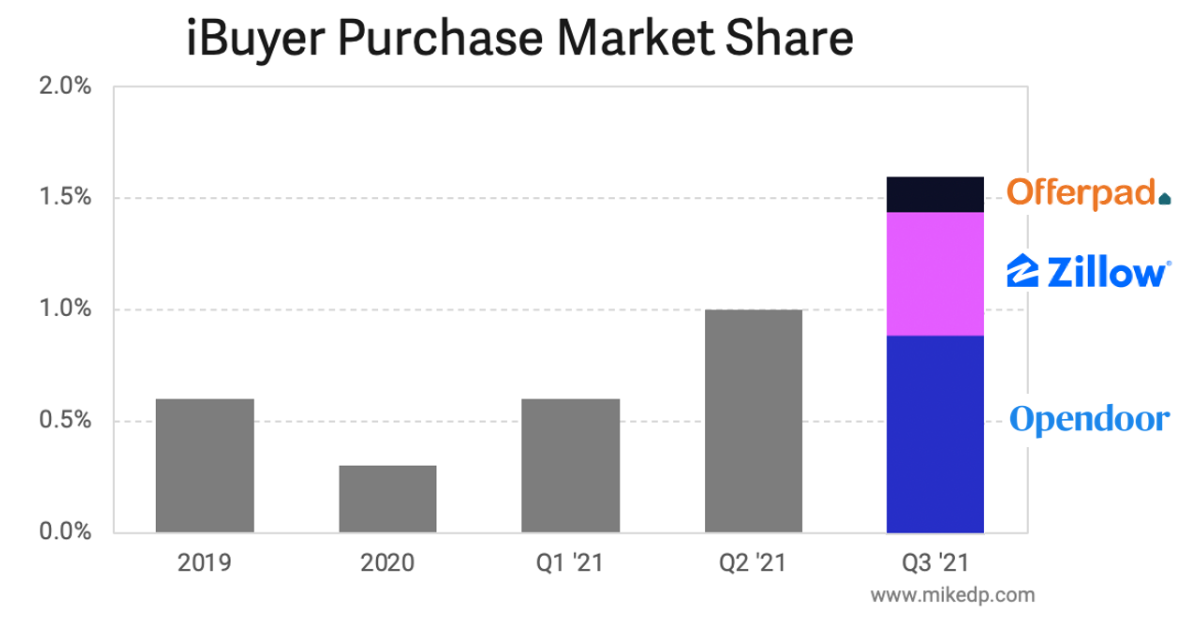

Although iBuyers collectively accounted for just 0.3 percent of U.S. existing home sales last year, according to BTIG, the rate of growth is worth watching. Opendoor, which went public in a SPAC merger last year, had drawn $1.8 billion on just under $4 billion in existing revolving credit facilities as of the end of June, according to Bloomberg.

Those numbers illustrate how hungry Opendoor is for homes. A separate analysis shows how its diet is changing.

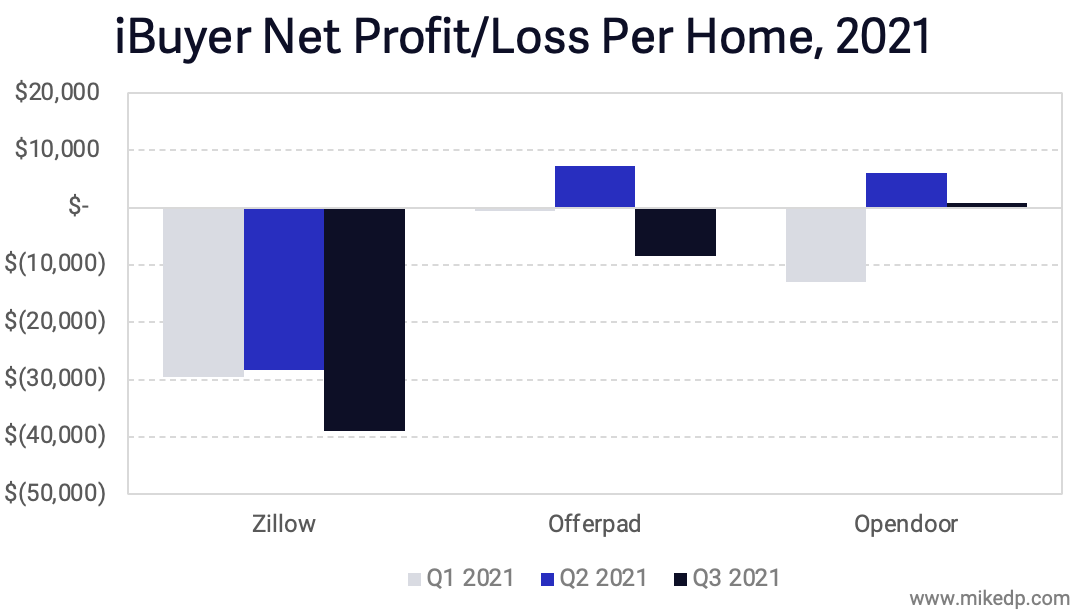

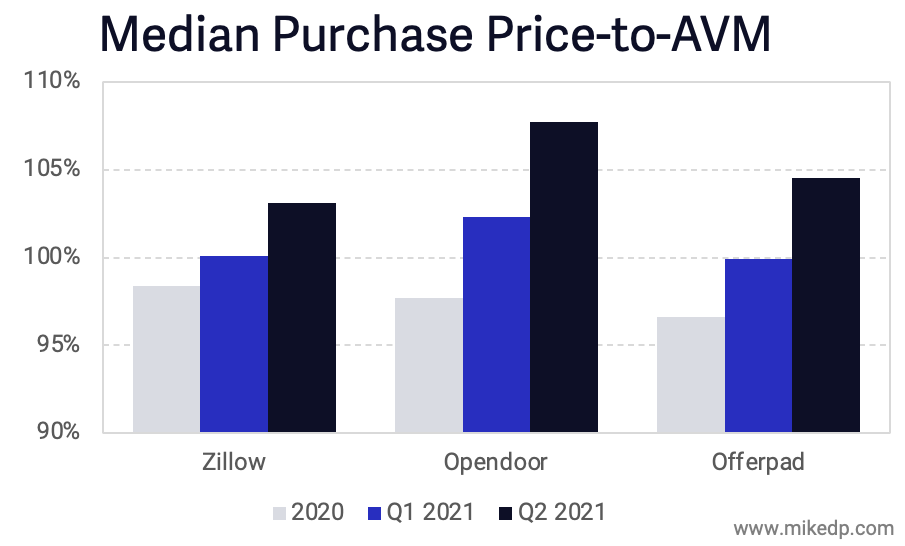

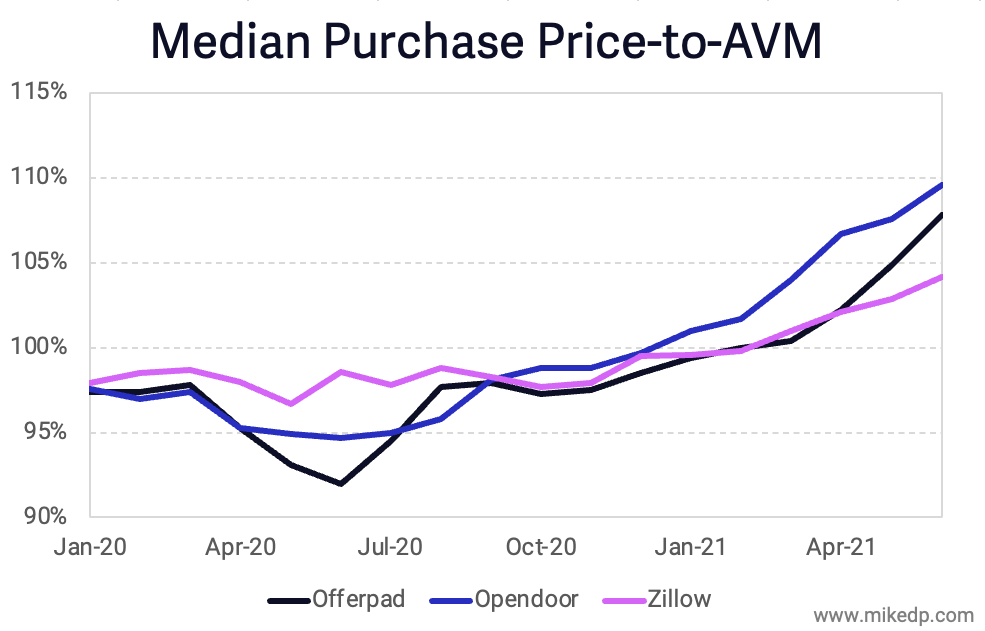

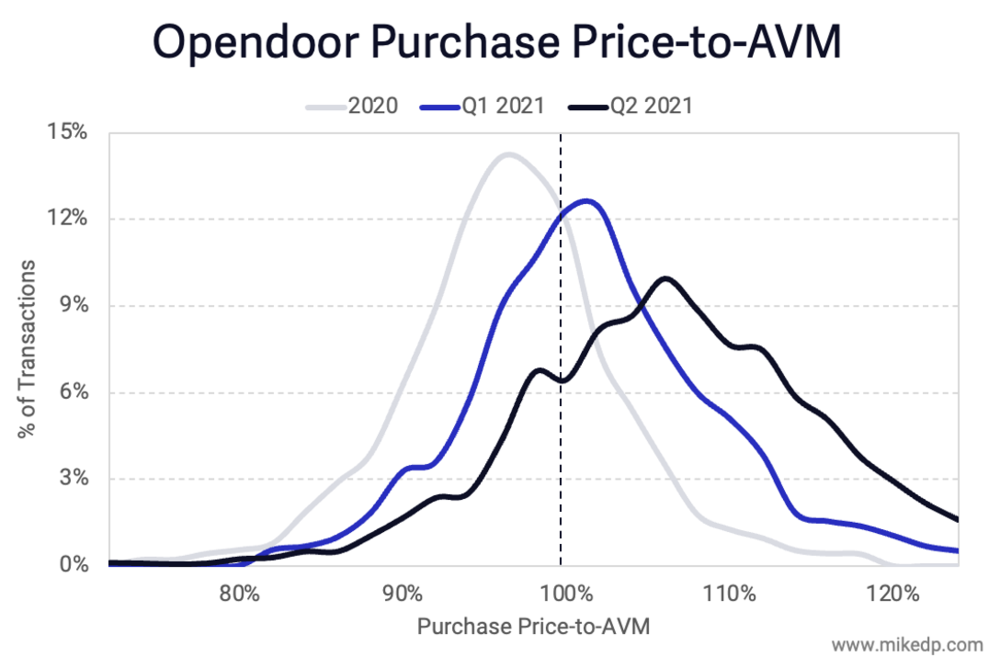

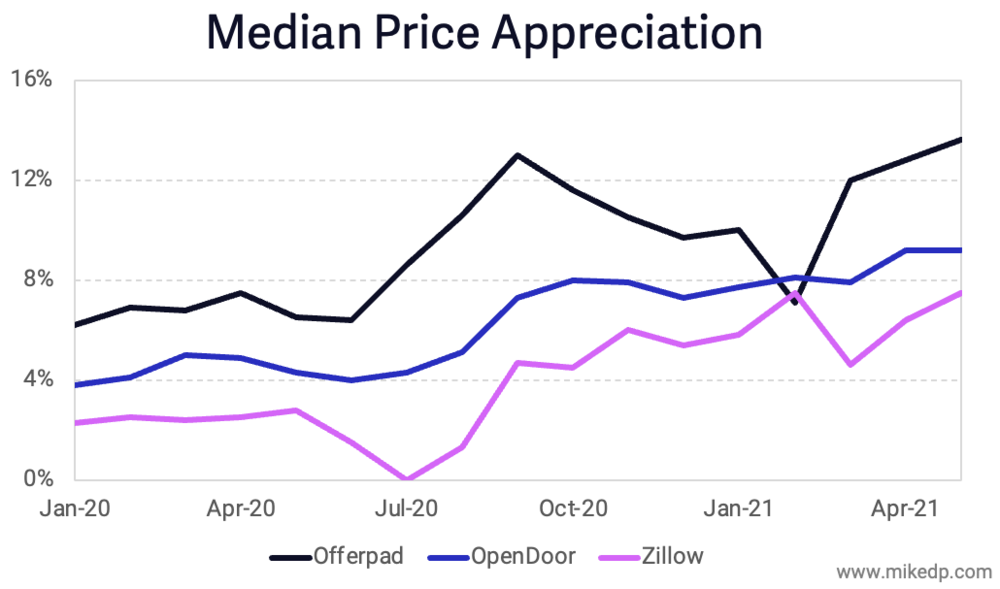

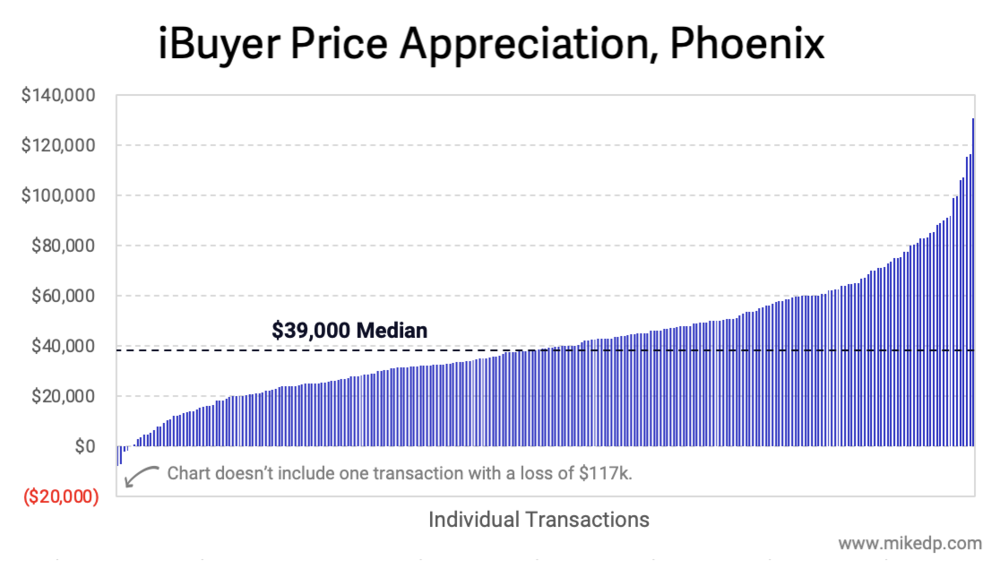

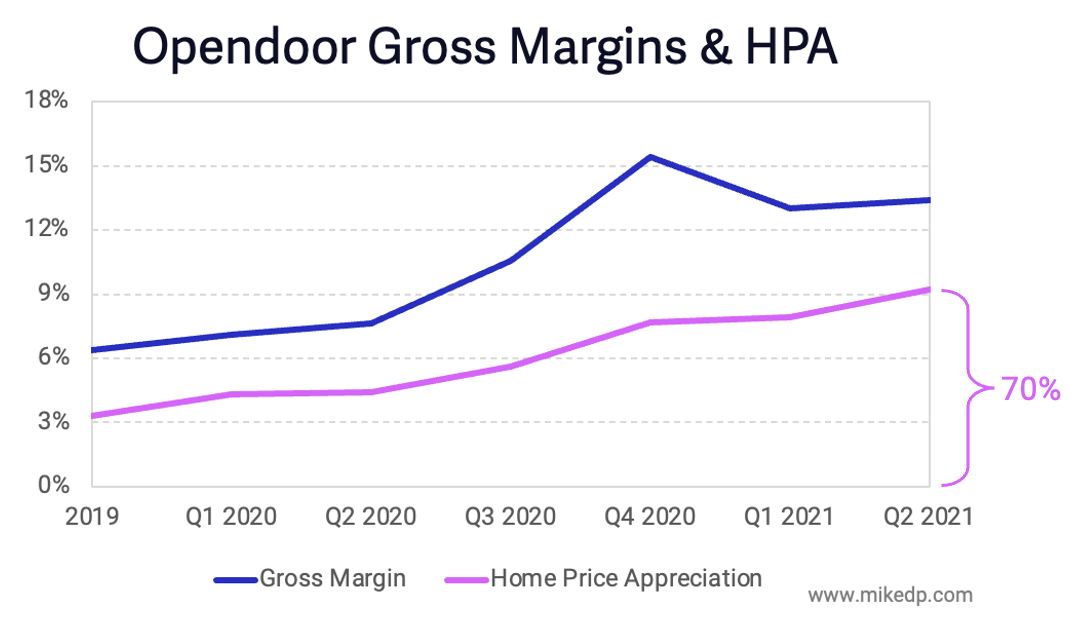

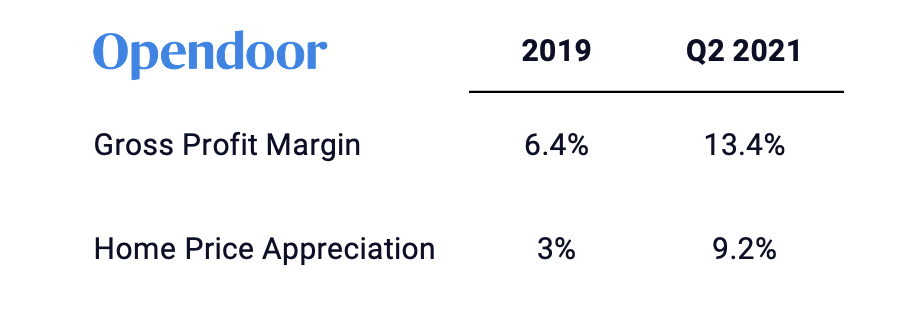

For several years, Opendoor and its two closest iBuying rivals, Zillow and Offerpad, had been buying homes with a median price of about $250,000, according to a study by industry analyst Mike DelPrete. In May, however, that median purchase price spiked to $350,000.

DelPrete attributed that 40 percent jump to the hot housing market. But he also noted that in the past 18 months, 24 percent of iBuyer purchases were of homes that cost more than $500,000, up from just 3 percent historically. So iBuyers are not only looking to buy more homes than ever before, they’re prepared to buy pricier ones, setting them up to compete with more aspiring homeowners.

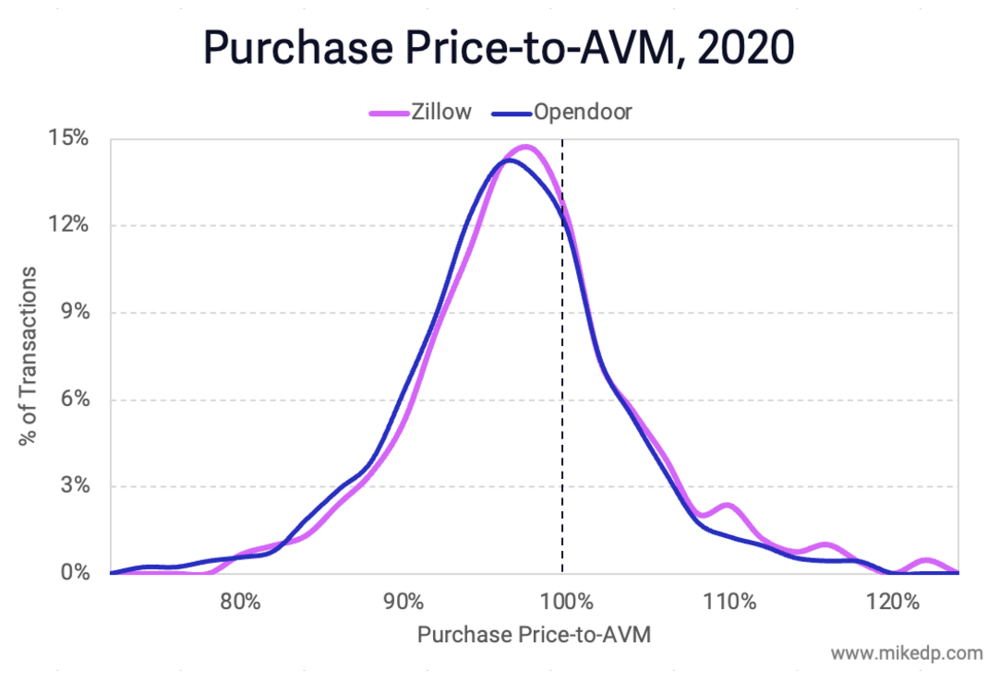

They’re no longer the discount buyer, either. Historically, Opendoor (and other iBuyers) paid a fraction below market rate for homes, compensating sellers for the haircut by

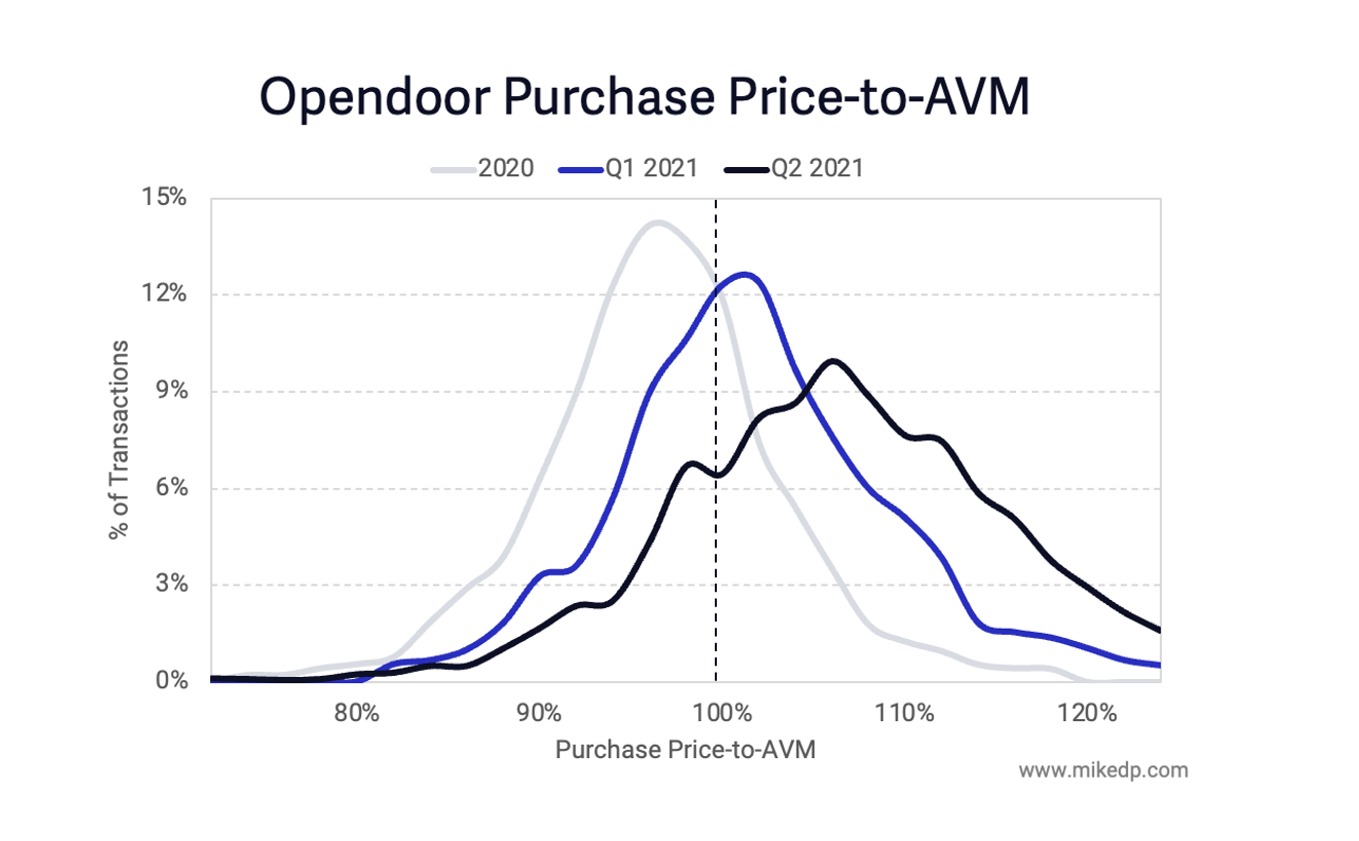

providing speed, certainty of closing and a hassle-free experience. Now, they’re willing to pay a premium to boost their holdings, DelPrete found, after comparing iBuyers’ purchase prices to those generated by property data provider Attom’s automated valuation model (AVM).

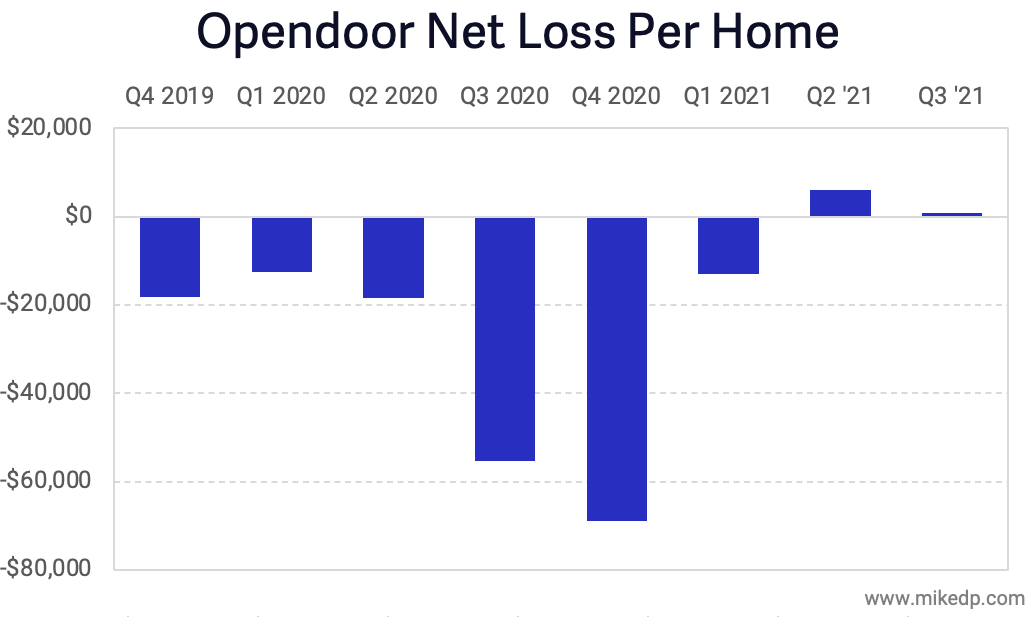

In the second quarter, Opendoor’s purchase price-to-AVM ratio was 107.7 percent. Bolstered by billions of dollars in revolving credit facilities and eager to show its investors major revenue growth, Opendoor seems happy to leave the bargain-hunting to others. That strategy isn’t without its risks: If the end of Covid-related forbearance does lead to a

wave of foreclosures, as some predict, the market could see a rush of supply, and iBuyers — and their investors — might find that they had overpaid.

For now, though, Opendoor and its competitors have a captive audience in single-family rental giants, who are making a huge bet that remote work, with its attendant demand for more residential space, will increase migration to the suburbs, and that high-earning millennials are more likely to prize the flexibility of renting over the anchors of homeownership. So far this year, the numbers certainly bear that out: Asking rents for professionally managed houses rose nearly 13 percent for the year to date through July, the highest annual increase in the past five years, according to Yardi Matrix data

cited by the Wall Street Journal.

iBuyers are selling more and more homes directly to such landlords, effectively bypassing the homebuyer market. Between 5 and 6 percent of Invitation Homes’ 700 first-quarter acquisitions came from iBuyers, Tanner said

during an April earnings call. The following month, during an

investor presentation, the company, which owns about 80,000 homes across 16 markets, said it was positioned to be the “buyer of choice” as the “iBuying market continues to grow.”

Recent comments by Doug Brien, CEO of Mynd, a property management firm catering to single-family rental investors, hint at this. Mynd plans to buy 20,000 homes across the U.S. over the next three years on behalf of Invesco, with a predicted price tag of $5 billion.

Up to a fifth of those homes,

Brien told Insider, would come through iBuyers.

“You have to be playing in every channel there is,” he said.

Customer-investors

At the top of a

June earnings call, Stuart Miller, executive chairman of Lennar, the nation’s largest homebuilder, took a long view on the booming housing market. He spoke of low interest rates and tight supply. Then he got to Opendoor.

The company and its peers, Miller said, “are becoming more than just a home sale option.” The value proposition offered by iBuyers, he explained, “is becoming the core of a coordinated closing without double moves or double housing costs.”

Miller was speaking as both a student of the housing market and a key backer of the startup.

Lennar provided Opendoor with $100 million in debt financing in January 2018 through a deal structured by its venture partner Fifth Wall. That June, Lennar also co-led Opendoor’s $325 million funding round. Another investor in that round? Invitation Homes.

Viewed as a straight investment,

Lennar’s bet paid off in spades when Opendoor went public through a merger with Chamath Palihapitiya’s blank-check firm in December 2020. But it’s clear that Lennar sees the iBuyer as more than a return: It’s treating the investment as a learning lab, testing various initiatives such as a trade-up program, in which homeowners buying a new Lennar house can sell their existing home to Opendoor, with the companies working to coordinate closings. Miller described Opendoor as a partner in facilitating “the fragile dance of selling an old home.”

Opendoor and Lennar have a trade-in partnership (Source: Opendoor)

Invitation Homes, too, sees iBuyers as petri dishes. In 2018, Tanner said they could help the company find new customers and create a sale-leaseback program, through which owners would sell their homes to the company and then rent them back until “they make their next life decision.” In September 2020,

the Journal reported that Invitation Homes had updated investors about the program, though the company insisted plans were still in the early stages.

In March, Lennar formed a single-family rental vehicle,

Upward America Venture, backed by institutional players such as Centerbridge and Allianz Real Estate. The vehicle hopes to acquire $4 billion worth of new homes and townhomes from Lennar and other builders, offering some up through a rent-to-own option.

“We have a distinct opportunity to create upward mobility in the housing market through this initiative,” Lennar co-president Rick Beckwitt said at the time. If it needs to figure out how to move fast, it may turn to Opendoor, creating another B2B channel for single-family homes.

Attachment theory

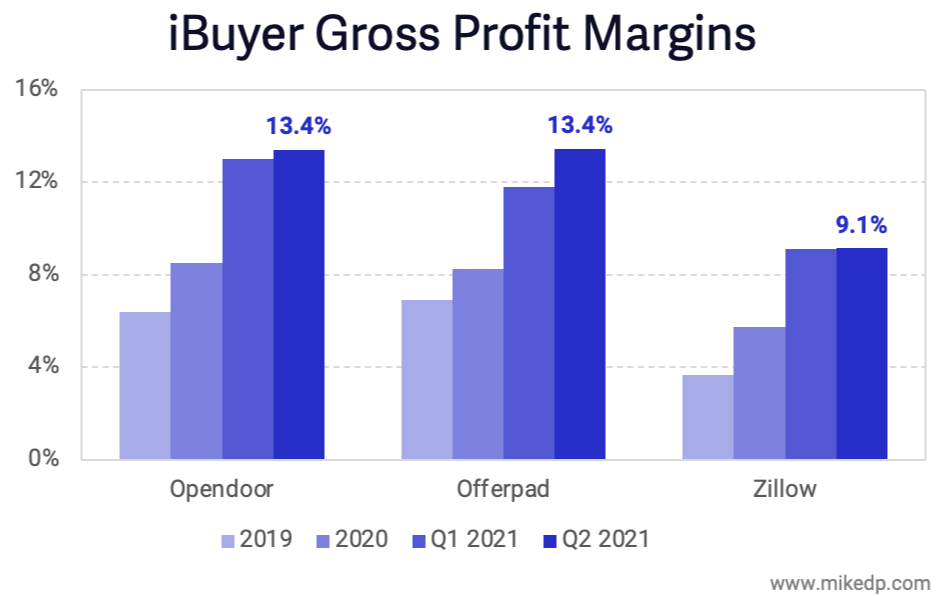

On Aug. 16,

Offerpad announced its first profitable quarter, reporting $9.2 million in net income, and disclosed a contribution margin — defined as the per-unit selling price less the variable cost — of $31,500 per home. (

The company went public this month, in a SPAC merger with Zillow co-founder

Spencer Rascoff’s Supernova Partners)

The dream scenario for iBuyers, however, isn’t simply making a profit on a home sale. Instead, it’s an ecosystem play, monetizing adjacent services such as title and escrow, mortgages and insurance. It’s those gains from packaging offerings together — known as the “attach rate” — that will really boost profitability. For example, according to its September 2020 investor presentation, Opendoor is targeting a contribution margin of $1,750 for title and escrow services and a contribution margin of $5,000 for mortgages.

")